How to Claim After a Non-Fault

Accident in the UK A Calm, Clear Guide

The bump was sudden. Your heart’s racing, traffic’s backing up, and your car—or taxi or bike—might be off the road. You’re asking the same questions everyone asks: Who pays? What do I do now? How do I get a like-for-like replacement without surprise bills? Breathe. This guide keeps it simple and human.

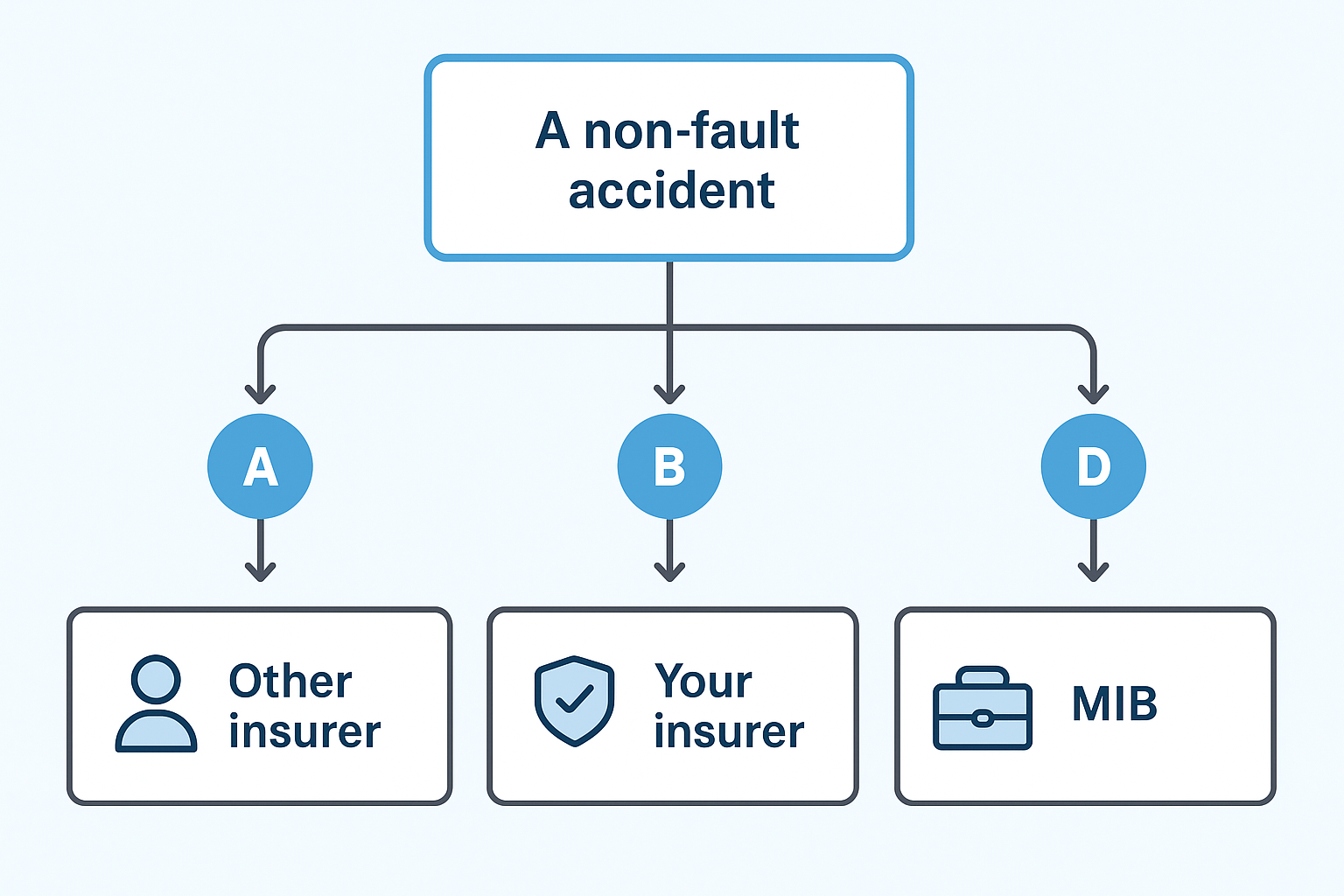

In the next few minutes, you’ll learn exactly what “non-fault” means, what to collect at the scene, and the four claim routes: your insurer, the other driver’s insurer, credit hire/accident management (with safeguards), or the MIB if they’re uninsured. You’ll also see a quick decision matrix to pick the best route for you.

In 2023, Great Britain recorded 132,977 road casualties, including 1,624 fatalities—sobering proof that clear steps matter in the moments after a crash According to the UK Department for Transport road casualties remain a major concern. At the same time UK motor claims costs reached record levels in 2024 and premiums remain under pressure. Getting the process right protects your time, money, and mobility.

The four routes at a glance

| Route | When it shines | Watch-outs |

|---|---|---|

| Direct to other driver’s insurer | Liability is clear; you want fewer middle steps | Repairer/control may be theirs; timelines vary |

| Through your insurer (still non-fault) | You prefer convenience and a single point of contact | Understand excess/NCD rules and admin impacts |

| Credit hire / Accident management | You urgently need like-for-like mobility (taxi/van/bike) | Hire class & duration must be reasonable; liability disputes risk |

| MIB (uninsured / untraced) | The at-fault driver is uninsured or fled | More forms; keep police ref & evidence tight |

A non-fault accident claim means the other driver (or their insurer) should pay your reasonable losses. Stay safe, collect evidence, report if required, then choose a route: your insurer, the other driver’s insurer, a credit-hire/accident-management service (with care), or the MIB if the other driver is uninsured.

What “non-fault” really means ?

“Non-fault” means your insurer (or an accident-management company) can recover costs from the other driver’s insurer. The incident can still be recorded on your insurance history, and while that’s not the same as losing your no-claims discount (NCD), premiums can reflect incident history.

- Citizens Advice : what happens when it wasn’t your fault: Read Here

- FOS on fault/non-fault dynamics (credit hire contexts): Read Here

Who pays?

Ordinarily, the at-fault insurer funds reasonable repairs, replacement hire (when justified), and associated losses. If the other driver is uninsured or untraced, use the Motor Insurers’ Bureau (MIB) process . “Reasonable” is assessed case-by-case—class of vehicle and hire duration must fit your real need.

ABI claimant guidance: https://www.abi.org.uk/globalassets/files/publications/public/motor/2022/third-party-assistance-claimant-guide.pdf

Myths to avoid

Myth: “Like-for-like replacement forever.”

Reality: Hire must be reasonable and aligned to repair/settlement timelines (FOS) Myth: “Non-fault never affects price.”Reality: The claim can be recorded; NCD differs from overall pricing (check your policy wording; see Citizens Advice pages above).

First 10 minutes after the accident

(safety, duties, evidence)

Make safe & exchange details.

Stop, make the scene safe, and exchange names, addresses, and registration numbers. Take photos from several angles, note road position/markers, and collect witness contact details.

When to report to the police?

If details aren’t exchanged, anyone is injured, or an offence is suspected, you must report. Use local police guidance if needed.

Build your evidence pack (save this list)

- Photos/video (vehicles, plates, road layout)

Time/date/location, weather

Other driver’s details + insurer

Witness names/numbers

Police reference (if any)

Medical notes/receipts; travel or tool hire receipts

Loss-of-use or income notes (especially for taxis/delivery riders)

Internal help, if you’re in England: To avoid storage drift, arrange rapid recovery & secure storage once safe—see: . For mobility, see like-for-like replacement options:

Evidence checklist (print this)

| Item | Why it matters | Tip |

|---|---|---|

| Photos/video | Proves damage, positions | Shoot wide, then close-ups |

| Witness details | Independent support | Save names + phone numbers |

| Police ref | Confirms reporting | Ask for incident reference |

| Expenses | Recoverable costs | Keep receipts, note dates |

| Income loss notes | Taxi/rider proof | Simple log: dates, hours, bookings missed |

Choose your claim route (pick the

best path for you)

1 . Claim directly from the other driver’s insurer

Good when liability is clear and you want fewer middle steps. Expect the other side to suggest their repairer; you can discuss alternatives. Keep your evidence tight and ask timelines in writing.

2 . Claim through your insurer (still non-fault)

Convenient if you want one point of contact. Understand how excess/NCD is handled in your policy; some insurers reclaim it later when the at-fault side pays. Keep your documents organised to speed subrogation.

3 . Use a credit-hire/accident-management service (with care)

Ideal when you urgently need like-for-like to keep working (PCO taxi, van, or bike). The key is reasonableness: vehicle class and hire duration must match your real need and repair/settlement timings. Keep updates and dates. If unhappy, you can escalate.

4 . If they’re uninsured or untraced: the MIB

Use the MIB route for uninsured or hit-and-run drivers. You’ll need strong evidence and, typically, a police ref.

MIB making a claim: https://www.mib.org.uk/making-a-claim

Decision Matrix — Which route fits?

| Factor | Direct to other insurer | Through your insurer | Credit-hire/AMC | MIB |

|---|---|---|---|---|

| Speed to start | 3/5 | 4/5 | 4/5 | 2/5 |

| Control over repairer | 3/5 | 2–3/5 | 4/5 | 2/5 |

| Like-for-like potential | 3/5 | 2–3/5 | 4/5 | 1/5 |

| Admin burden | 3/5 | 4/5 | 4/5 | 2/5 |

| Best for | Clear liability | Simplicity | Urgent mobility | Uninsured / hit-and-run |

Need Internal Help?

Internal help, if you’re in England: Need wheels fast? Explore like-for-like replacement options (taxis/PHV, vans, bikes): https://accidentassistnetwork.co.uk/replacement-vehicles . Prefer to speak first? Contact: https://accidentassistnetwork.co.uk/contact-us .

Replacement vehicle & repairs (how to stay

mobile without headaches)

Like-for-like vs reasonable

You should be put back into a broadly similar position—often a like-for-like vehicle. But courts and ombudsmen judge reasonableness: don’t keep a prestige car if a standard car meets your need; match hire length to repair/settlement timing.

FOS (reasonableness): https://www.financial-ombudsman.org.uk/…/credit-hire-credit-repair-services-following-no-fault-accident

ABI claimant guide: https://www.abi.org.uk/globalassets/files/publications/public/motor/2022/third-party-assistance-claimant-guide.pdf

Repairs, total loss & complaints

Repairs should meet manufacturer standards. If your vehicle is a total loss, valuations can be negotiated—keep adverts/valuations as evidence. If you’re unhappy, use the firm’s complaints process; escalate to the Financial Ombudsman Service if unresolved.

Storage fees & delays

Avoid spiralling storage costs by arranging recovery and secure storage promptly and moving to an appropriate repairer once authorised: https://accidentassistnetwork.co.uk/recovery-storage . Keep dated notes of any parts delays or missed appointments—documentation supports reasonableness.

Documents, time limits & quick FAQs

Create a folder with sub-folders: Photos/Video, Witnesses, Police, Medical, Expenses, Vehicle, Hire/Repair Updates. Save emails as PDFs. Keep a simple expense log: date, item, amount, receipt.

Simple documents map

| Document | Where it’s used | Tip |

|---|---|---|

| Photos/video | Liability, repair assessment | Back up to cloud same day |

| Receipts/expenses | Recovery of out-of-pocket costs | Label files “YYYY-MM-DD_item” |

| Hire/repair updates | Reasonableness of duration | Keep a dated timeline |

| Income loss notes | Taxis/delivery riders | Export weekly summaries |

Conclusion: your next steps

Calm, then act.

Accidents are stressful, especially if your wheels equal your income. With a solid evidence pack and the right route, you can recover your reasonable losses, keep moving, and reduce admin. If the other driver was uninsured, the MIB route exists—just keep your documents tight: https://www.mib.org.uk/making-a-claim .

Need practical help in England?

If you’re in England and need recovery, secure storage, or a like-for-like taxi/van/bike while repairs are arranged, the Accident Assist Network team can coordinate in plain English (also explained in Romanian/Urdu/Tamil/Hindi). “1 Call, we sort it all.”

Replacement vehicles (priority): https://accidentassistnetwork.co.uk/replacement-vehicles

Recovery & storage: https://accidentassistnetwork.co.uk/recovery-storage

Repairs: https://accidentassistnetwork.co.uk/vehicle-repairs

Quick poll (help us help you):

Which route fits your situation today?

What is a non-fault accident in the UK?

Who pays after a non-fault crash?

Should I claim via my insurer or the other driver’s insurer?

What is credit hire, and what are the risks?

Do I have to use their repairer?

How long do I have to claim?

Compliance & service footprint note

This guidance is UK-general to help readers, but Accident Assist Network services are delivered in England (London-first). We coordinate vehicle-damage support only and do not provide legal advice.