let’s start where you are

You’re okay, but your motorbike isn’t. You’re staring at a bent lever, a cracked fairing, and a silent question: what now? A bike insurance claim sounds simple—until fault, NCD, valuations, and timelines turn into a maze. You want your wheels back, a fair outcome, and zero jargon.

what this guide does for you

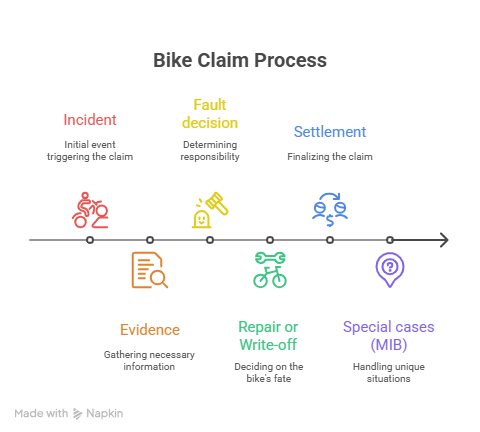

In clear English, we’ll map the route: what counts as fault vs non-fault, how a bike insurance claim actually moves, how to build an evidence pack, when MIB applies, and how to challenge a low write-off offer. You’ll see the steps. You’ll know your options.

facts that change the conversation

UK motor insurers paid a record £11.7bn in 2024—pressure that still shapes how claims are handled in 2025 (ABI news). Regulators also forced ~£200m in compensation where payouts for stolen/write-off vehicles were undervalued (Reuters, FT). Translation: if an offer feels wrong, you’re not imagining it.

A bike insurance claim (motorbike, England) is the process of getting your damaged bike repaired or fairly compensated after a crash. Collect evidence, report the incident, and choose the correct route: your insurer, the at-fault insurer, or (if uninsured/untraced) the MIB. Build a valuation pack and challenge low offers using market-value proof.

What to do in the first 24

hours

1) Secure the scene and capture proof

Safety first. Photograph damage, road conditions, and positions from multiple angles. Save dashcam clips. Note time, location, weather, and plate numbers. Capture riding-app bookings or job logs if you’re a delivery rider—these help show practical need for mobility.

2) Exchange and record

Swap names, addresses, registrations, and insurer details. If police attend, note the incident reference. Keep a claim log with dates and the name of every person you speak to.

3) Notify and choose your route

Report promptly. If you’re clearly non-fault, consider engaging the at-fault insurer or an independent route that can coordinate recovery, secure storage, repairs, or like-for-like hire (eligibility applies). The aim is to keep your bike insurance claim organised and moving.

4) Think ahead about mobility

Delivery riders: note your next shifts and regular routes. These facts help justify like-for-like replacement usage (where appropriate) and keep your documentation consistent later.

Fault vs non-fault and

what that means for your

NCD

What “fault” really means

“Fault” isn’t a moral label. It’s an insurer’s record about who pays. If there’s no recoverable third party (e.g., diesel spill, unidentified driver), a claim may be recorded as fault, which can affect NCD unless protected. Always ask your insurer how your bike insurance claim will be coded.

Non-fault clarity

When another motorist is clearly responsible and their insurer pays, your NCD is typically protected—but timing matters. If your own insurer pays first and later recovers the outlay, the record can change. Expect admin lag before everything lines up.

Edge cases riders face

Untraced driver: hit-and-run or no details—consider MIB for property damage if eligible (GOV.UK, MIB). GOV.UK+1

Road defects/contamination: spills or potholes complicate liability—document conditions thoroughly and keep all references.

Keep the conversation factual. Ask your insurer to confirm in writing how this bike insurance claim will be recorded and what that implies for renewal.

Build your evidence pack — the fast track to fair outcomes

Core set for every rider

Photos/video of all angles, close-ups, and the wider scene

Your details, third-party details, witness contacts

Service history, receipts, security devices, modification list

Delivery riders: booking screenshots, shift logs, top-box/helmet details and proof of day-to-day usage

The valuation dossier

Low offers are not rare. Regulators have confirmed industry-wide issues with under-valuation on total-loss claims; firms are revising methods and paying compensation (FCA review, FT coverage). Build your case: 4–6 like-for-like ads with mileage/condition, service proof, and high-res images. FCA+1

How to challenge a low write-off valuation (copy these steps)

Keep it short and polite.

Attach your comps list and explain each comp’s mileage, year, and spec.

Ask for a reassessment with a written breakdown of the figure used.

If unresolved, escalate via the insurer’s complaints process and then the Financial Ombudsman Service (consumer guidance on write-offs and valuations is here: FOS). Financial Ombudsman

Write-off categories & DVLA steps (Cat S/N)

Cat S means structural damage; N means non-structural. Both can sometimes return to the road, subject to proper repair and paperwork. GOV.UK explains what each category means and what to do with your V5C after a write-off (write-offs & DVLA).

Repairs vs write-off — decisions, timelines, and practical choices

How the decision is made

An insurer compares the estimated repair cost with the bike’s pre-accident value (PAV), minus salvage value. If repair costs exceed that threshold, it’s usually a write-off—an approach reflected in official guidance and industry practice (UK guide note on write-offs). GOV.UK

If your offer feels low

Return to your valuation dossier. Ask them to consider your specific extras (heated grips, luggage systems) and service history. Link to your comps and request their method statement in writing. If they won’t budge and you believe it’s below fair market value, consider escalating to FOS with your evidence set (FOS approach). Financial Ombudsman

Managing the downtime

Parts delays can stretch timelines. Keep polite, dated chaser emails every 5–7 days. Delivery riders: log lost shifts and reasonable travel alternatives you’re using—this keeps your bike insurance claim documentation clear and consistent.

Where AAN fits naturally (non-fault)

When your crash is non-fault, coordinated recovery, secure storage, manufacturer-standard repairs, or like-for-like replacement motorbikes may be available through independent partner networks. That’s where a practical, friend-first coordinator adds value—without hype, just organisation and clarity.

Uninsured or untraced third-party — when the MIB route applies

If there’s no insurer to recover from (uninsured driver or hit-and-run), you may claim through the Motor Insurers’ Bureau for property damage, subject to the Uninsured/Untraced Drivers’ Agreements. Expect documentation, timelines, and specific eligibility rules (GOV.UK overview, MIB ‘claiming against an uninsured driver’, MIB ‘what we do’). GOV.UK+2mib.org.uk+2

What you’ll likely need

Police incident reference and, if applicable, crime number

Photos/video, witness details, and any dashcam footage

Repair/valuation evidence or write-off documentation

A clear timeline of events and correspondence history

Stay realistic. MIB isn’t a shortcut; it’s a route when normal recovery is impossible. Set expectations early and keep copies of everything.

Replacement mobility (non-fault) — like-for-like basics

Why it matters

For a commuter or courier, a week off the road isn’t just inconvenient—it can break routines and income. Where non-fault is clear and the situation is suitable, like-for-like replacement bikes may be arranged so you can keep moving while your bike insurance claim progresses.

Use it responsibly

Stick to normal usage, keep mileage reasonable, and store the bike safely. Keep a short usage log if you’re a delivery rider—dates, hours, and platforms. It helps if questions arise later.

AAN’s natural role

If your crash was non-fault and you need recovery, secure storage, repairs, or like-for-like motorbike hire coordinated quickly (subject to eligibility), Accident Assist Network can help as a friendly first call—London-first, across England. See our page for bikers & delivery riders.

Service note & Mandatory Disclaimer

Accident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If the at-fault insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Please read every document thoroughly and, if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.

Need practical help in England?

Call: 020 4577 1120 · WhatsApp: 07585 300 600

FAQS

If the other party’s insurer pays, NCD is typically protected. But if there’s no recoverable third party (e.g., untraced driver), the claim can be recorded as fault, impacting NCD unless protected. Always ask your insurer how your bike insurance claim will be coded and later adjusted.

Share your valuation dossier (4–6 comparable ads with mileage/spec) and request a written reassessment. If unresolved, escalate via the insurer’s complaints process and then the Financial Ombudsman Service (FOS consumer guidance).

Cat S is structural damage; N is non-structural. GOV.UK explains what happens to your V5C and your options after a write-off (write-off guidance).

Use MIB when there’s no insurer to recover from (uninsured or hit-and-run) and your situation fits the Uninsured/Untraced Drivers’ Agreements (MIB ‘uninsured driver’).