Non-Fault Accident Premium Rise Explained UK (2026)

Non-fault accident renewal worry? Learn why premiums can rise, how NCB differs from price, what evidence to keep, and when to call 020 4577 1120 today.

🔍 QUICK ANSWER

A non-fault accident can still affect your insurance renewal because insurers may record the incident in your claims history and price risk separately from blame.

- Your no-claims bonus is not the same as your final renewal price.

- Your excess position depends on how the claim route works and whether costs are recovered.

- Liability and claim status matter, especially if the claim is still open.

- Evidence helps you challenge unclear records, but it cannot control insurer pricing.

- Start by separating blame, record, recovery and renewal price.

Had a non-fault accident and unsure what to do next?

Call 020 4577 1120 or WhatsApp 07585 300 600 for practical vehicle-damage guidance across England.

Because Asking is the first step

What does Accident Assist Network do and how can it help me right now?

That support keeps the focus on your damaged vehicle, not insurance pricing advice.

Learn how Accident Assist Network supports drivers after an accident →

🎬 Watch the non-fault accident premium rise guide for UK drivers

Watch for a clear overview of why premiums can rise, how NCB differs from price, what evidence to keep, and when to call for help.

Because Asking is the first step

How does Accident Assist Network coordinate my non-fault claim with the at-fault driver's insurer on my behalf?

This can reduce practical confusion while keeping the support focused on vehicle damage only.

Understand non-fault accident claim coordination →

You were told it was a non-fault accident, so the renewal quote felt like it should stay simple. Then the price changed. That can feel unfair, especially when you did not cause the crash. You may be asking whether your no-claims bonus is safe, whether you should have claimed differently, and what your insurer has recorded. This guide breaks the problem into clear parts for private motorists, family drivers, open-claim drivers and professional drivers, so you can ask better questions before renewal and avoid guessing your way through the process.

Need help separating excess, no-claims bonus, repair options, and replacement transport?

Call 020 4577 1120 or WhatsApp 07585 300 600 for a calm vehicle-damage assessment.

Why Can Premiums Rise?

Why does a non-fault accident affect renewal?

A non-fault accident can affect renewal because insurers may treat accident history as part of risk pricing. That does not mean you were blamed. It means the incident may still sit in your claims history when your next policy price is calculated.

“Non-fault” usually answers one question: who was responsible for the accident costs. It does not mean the incident disappears from your insurance record.

This is where many drivers feel caught out. You may have done everything correctly, reported the incident honestly, and still find the accident listed when you compare renewal quotes. GOV.UK says that after an accident causing damage or injury, you must provide details to anyone with reasonable grounds to ask, such as an insurance company, and must report the accident to the police within 24 hours if details were not exchanged at the time.

The clearest way to understand the issue is to split it into four questions:

Data layer

| Question | Plain-English Meaning | Why It Matters |

|---|---|---|

| Who was to blame? | Which driver caused the accident? | Helps determine liability. |

| How is it recorded? | What your insurer or database shows. | Affects future quote questions. |

| Were costs recovered? | Whether the paying insurer recovered outlay. | Can affect claim status. |

| What is the renewal price? | The final policy price after underwriting. | Separate from blame and discount. |

The Association of British Insurers reported that motor insurers paid £11.9 billion across 2.5 million motor claims in 2025, showing the wider claims-cost pressure behind current pricing sensitivity.

Bridge: Once you separate blame from renewal price, the next confusion is usually the no-claims bonus.

Does Non-Fault Protect NCB?

Can no-claims bonus stay but price rise?

Yes. Your no-claims bonus can remain in place while your overall insurance renewal still rises. That is because your no-claims bonus is a discount mechanism, while the premium is the full price calculated after wider risk and market factors.

This is one of the most common misunderstandings after a non-fault accident. Many drivers think protected no-claims bonus means the whole renewal price is protected. It usually does not work like that.

The Financial Ombudsman Service explains that a “fault” claim can include a situation where the accident was not the driver's fault, but the insurer cannot recover the cost from another party. It also explains that a fault claim is likely to reduce no-claims bonus if it is not protected.

A Financial Ombudsman decision also records wording explaining that protected no-claims bonus does not protect the overall policy price, and that the policy price may increase after an accident even when the driver was not at fault.

Data layer

| Term | What It Means | Common Mistake |

|---|---|---|

| No-claims bonus | A discount linked to claim-free history. | Thinking it controls the whole price. |

| Protected no-claims bonus | A paid feature that may protect the discount. | Thinking it freezes renewal cost. |

| Premium | The actual insurance price. | Thinking it only rises after fault. |

| Base premium | The price before discounts apply. | Forgetting it can still change. |

If the base premium rises, the same discount can still leave you paying more. That feels frustrating, but it is different from losing your no-claims bonus.

Bridge: The next issue is timing. If your claim is still open, renewal can become even harder to understand.

What If The Claim Is Open?

Can an open claim affect renewal timing?

An open claim can affect renewal because liability, cost recovery or claim classification may not yet be final. Your insurer may still be waiting to recover costs or confirm fault, so the incident can appear differently at renewal than it does later.

A claim can feel “non-fault” to you from the start. The other driver may have apologised. The damage may clearly show what happened. But insurers work with records, evidence and recovery.

If the at-fault insurer has not accepted liability, if repair invoices are still being processed, or if costs have not been recovered, the claim may remain open. That can affect how your no-claims bonus, excess and claim status are shown at renewal.

The Financial Ombudsman Service states that fault recording can depend on whether costs can be recovered from another party, not only on who caused the accident.

Data layer: Claim Status Glossary

| Claim Status | What It Usually Means | Question To Ask |

|---|---|---|

| Notification-only | You reported the incident, but no payment was requested. | “Is this recorded as notification-only?” |

| Open claim | Liability or recovery is not finished. | “What is still outstanding?” |

| Settled non-fault | Costs were recovered or liability was resolved. | “Can I have written confirmation?” |

| Disputed | The other side has not accepted responsibility. | “What evidence is needed?” |

| Fault record | Costs cannot be recovered from another party. | “How does this affect my NCB?” |

Fictional scenario: imagine a family driver whose parked car is hit while they are at work. The other driver leaves details, but the insurer has not recovered repair costs by renewal week. The driver may feel punished, even though the real issue is unresolved recovery timing.

Bridge: When timing matters, the route you choose after the accident becomes more important.

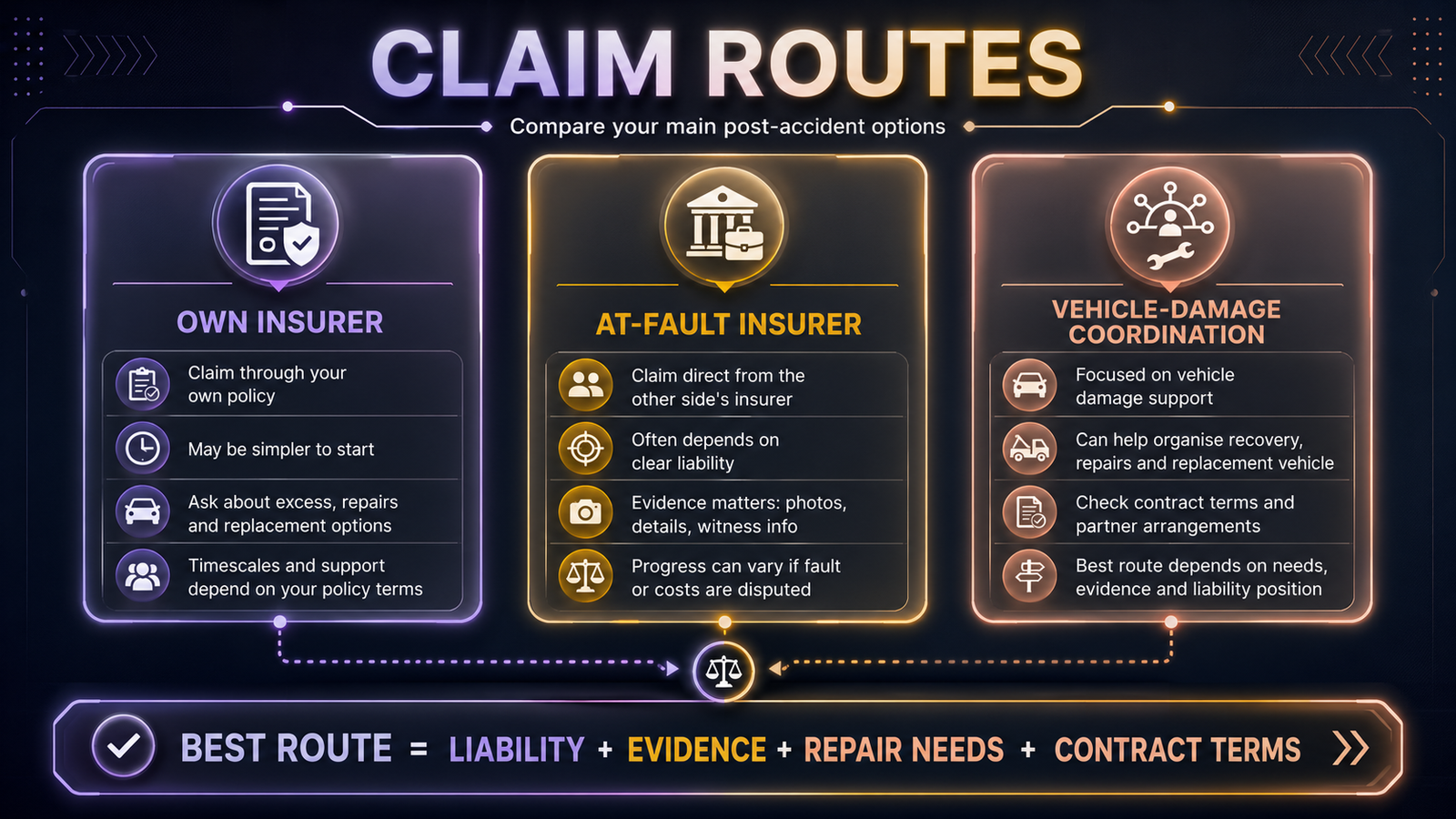

Which Claim Route Fits?

Should you use your insurer first?

After a non-fault accident, you may report the accident, claim through your own insurer, deal with the at-fault insurer, or use a vehicle-damage coordination route. Each option has benefits and limitations, so the right choice depends on liability, evidence, vehicle need and contract terms.

You should not hide an accident from your insurer. The real decision is usually about how the vehicle damage is handled after the incident has been reported.

Citizens Advice explains that if the accident was not your fault, you may be able to claim from the other driver's insurer. It also explains that credit hire can be used in some situations, but readers should check the agreement carefully because costs may be in their name.

Citizens Advice also advises keeping copies of documents and letters when making a claim after an accident.

Data layer: Route Comparison

| Route | What It Can Help With | What To Watch |

|---|---|---|

| Own insurer | Familiar process and policy route. | Excess may apply; claim may stay open until recovery. |

| At-fault insurer | Direct repair or hire route if liability is accepted. | Their priority may be cost control. |

| Vehicle-damage coordination | Recovery, storage, repairs and replacement hire through partners. | Read partner terms, especially credit-service liability. |

Accident Assist Network fits only in the practical vehicle-damage coordination space. It does not set renewal prices, give financial advice, provide legal advice, or make medical assessments. Its role is to help you understand and coordinate recovery, repairs, replacement hire and total-loss support through independent partner companies where suitable.

Bridge: The safer your evidence is, the easier it becomes to discuss fault, recovery and renewal clearly.

What Evidence Protects You?

What proof helps after a non-fault accident?

The best evidence pack shows what happened, who was involved, what damage occurred, what was reported and how the claim is currently recorded. It cannot control your renewal price, but it can help reduce confusion about liability, excess and claim status.

Evidence is not just for the roadside. It matters weeks later when you compare renewal quotes, ask your insurer for claim status, or query why a no-claims bonus appears different.

Your goal is not to argue emotionally. Your goal is to ask clear questions with documents in front of you.

Build one folder with:

- Accident date, time and location.

- Photos of vehicle position and damage.

- Registration numbers and driver details.

- Witness details, if available.

- Dashcam footage, if available.

- Police reference, if applicable.

- Claim reference and insurer correspondence.

- Repair, recovery or storage documents.

- Written claim status from your insurer.

- Any confirmation of liability or cost recovery.

Quotable insight: A non-fault accident is not one question. It is blame, record, recovery and renewal price.

For private motorists, this evidence helps when comparing quotes. For family drivers, it helps keep the household decision clear. For professional drivers, it helps protect work continuity discussions without drifting into unsupported claims.

Bridge: With evidence organised, you can ask your insurer better questions before renewal pressure builds.

What Should You Ask?

How can you prepare before renewal?

Before renewal, ask your insurer how the accident is recorded, whether liability is accepted, whether costs have been recovered, whether your excess is still outstanding and whether your no-claims bonus changed. Written answers are more useful than vague phone explanations.

A renewal quote can feel final, but you can still ask for clarity. You are not asking the insurer to ignore the accident. You are asking them to explain how it is recorded and priced.

Use this script:

| Your Question | Why It Matters |

|---|---|

| “Is the incident recorded as non-fault, fault, disputed or notification-only?” | Clarifies the claim label. |

| “Has the at-fault insurer accepted liability?” | Shows whether the record is settled. |

| “Have all costs been recovered?” | Explains whether it may still affect NCB. |

| “Has my no-claims bonus changed?” | Separates discount from price. |

| “Has the base premium changed?” | Explains why price rose despite NCB. |

| “Is any excess still outstanding?” | Clarifies practical cost exposure. |

| “Can you confirm this in writing?” | Gives you a record for comparison. |

If you drive for work, add one more question: “Does this record affect my business-use or licensed-vehicle cover?” For taxi, private hire and courier drivers, vehicle downtime can affect income and licensing suitability, so the replacement route matters.

I'm a Private Motorist and My Renewal Quote Rose After a Non-Fault Accident — Can Accident Assist Network Help?

Yes. If your concern started with a non-fault accident and vehicle damage, Accident Assist Network can explain practical recovery, repair, replacement hire and total-loss coordination options through partner companies.

You still make your own insurance decisions, but you do not need to untangle vehicle logistics alone.

Interactive Reflection

Which concern best describes your situation today?

- My renewal premium increased after a non-fault accident.

- I do not understand my no-claims bonus.

- My claim is still open.

- I paid excess and want clarity.

- My vehicle is still damaged or off the road.

- I drive for work and need practical continuity.

Write down your top concern before calling anyone. That one line will keep the conversation focused.

🎯 Your Next 3 Moves

Immediate: Save every accident, insurer, renewal, repair and recovery document in one folder.

This session: Ask your insurer how the accident is recorded and whether liability or cost recovery is complete.

This week: If your vehicle is still damaged, ask Accident Assist Network about practical recovery, repair or replacement coordination before signing any agreement.

Sources & References

- Source: GOV.UK — Vehicle insurance if you're in an accident. (gov.uk)

- Source: Financial Ombudsman Service — Fault claims and no-claims bonuses. (Financial Ombudsman)

- Source: Financial Ombudsman Service decision reference — Protected no-claims bonus and overall policy price. (Financial Ombudsman)

- Source: Citizens Advice — Vehicle insurance if the accident was not your fault. (Citizens Advice)

- Source: Citizens Advice — Making a vehicle insurance claim after an accident. (Citizens Advice)

- Source: Association of British Insurers — 2025 motor claims payout data. (ABI)

Want your vehicle-damage options explained before you sign anything?

Call 020 4577 1120 or WhatsApp 07585 300 600 for clear, friendly guidance.

Accident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles, and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Your one call and we sort it all.

Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme.

Our partner companies will always endeavour to help you recover costs from the at-fault insurer; however, if that insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Each partner company will supply its own terms and conditions in agreements. Please read every document thoroughly and, if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.

Need practical help in England? Call 020 4577 1120 | WhatsApp 07585 300 600

Frequently Asked Questions

Does a non-fault accident affect insurance renewal?

Do I have to declare a non-fault accident?

Can my no-claims bonus stay but my premium rise?

What happens if the other insurer disputes liability?

Do I pay excess after a non-fault accident?

Can Accident Assist Network change my renewal price?

What evidence should I keep after a non-fault accident?

What happens if the other driver's insurer disputes fault — will I end up with a bill from Accident Assist Network?

Because Asking is the first step

I’m a private motorist and my renewal quote rose after a non-fault accident — can Accident Assist Network help me understand my vehicle damage options?

You still make your own insurance decisions, but you do not need to untangle vehicle logistics alone.

See support for car and van drivers →

Still unsure what your non-fault accident means for your damaged vehicle?

Call 020 4577 1120 or WhatsApp 07585 300 600. Accident Assist Network can explain practical next steps across England, without pressure and with clear service-scope limits.

Raheel A Rathore

Directs Accident Assist Network, bringing 15+ years of practical UK motor claims coordination experience across England. Research support from Shahzeb.