Quick Answer: Does a Non-Fault Accident Affect Insurance?

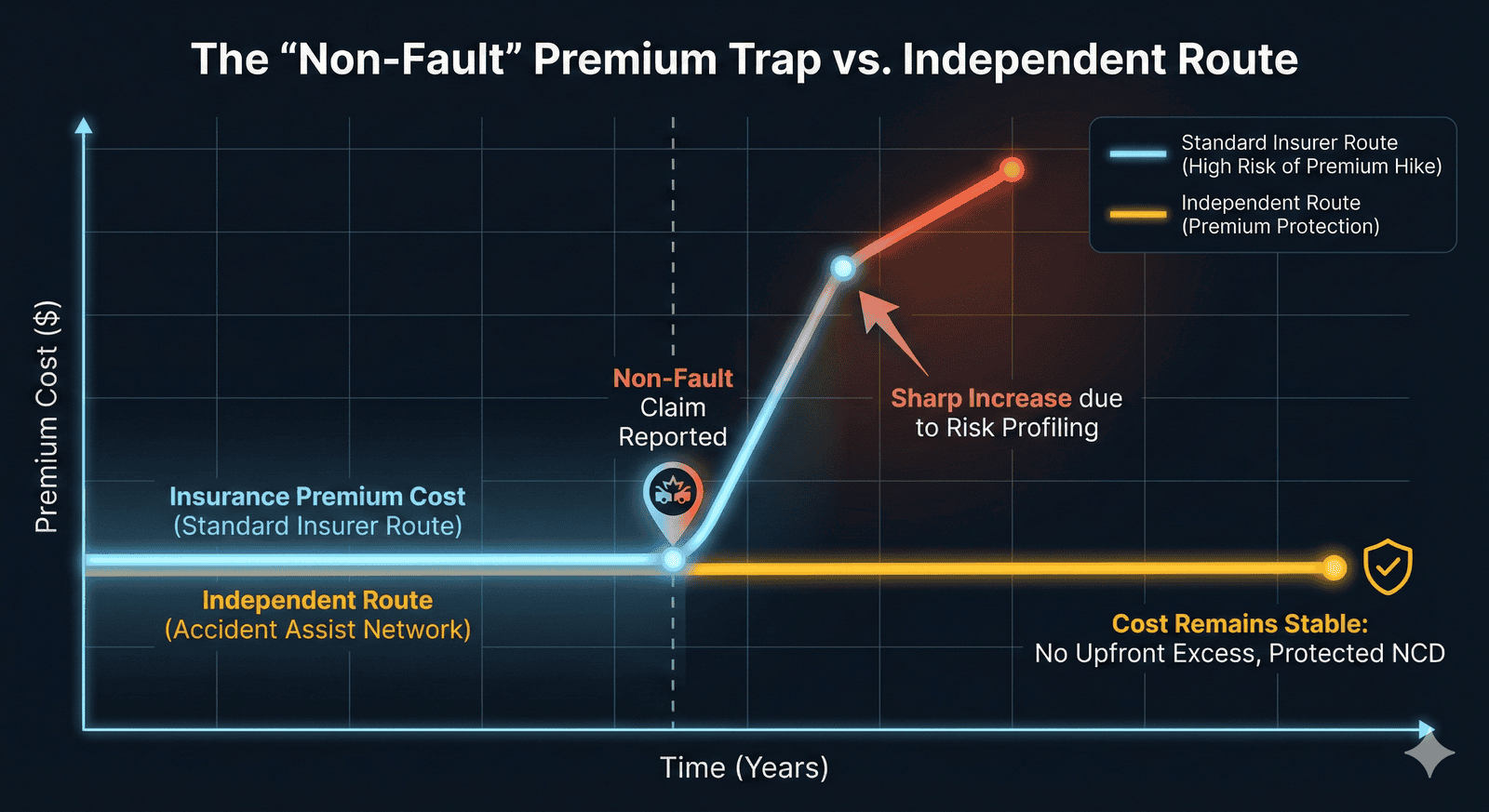

Yes. Industry data indicates that car insurance premiums can rise by up to 15-20% following a non-fault accident. This is due to "risk profiling," where insurers statistically view any involvement in an accident as an indicator of higher future risk.

How to stop it: To protect your No Claims Bonus (NCB) and avoid upfront excess fees, drivers can use independent claim coordination services to handle the claim directly against the at-fault driver's insurer, rather than claiming through their own policy.

The 2026 Insurance Trap: Why a "Non-Fault" Crash Could Still Cost You Thousands (And How to Stop It)

The Crash Was Bad. The "Admin Crash" is Worse.

"It wasn't my fault." It is the most frustrating phrase you can say while standing on the side of a wet road in London. You did everything right—you signaled, you checked your mirrors, and you drove carefully—yet someone else’s mistake has just taken your vehicle off the road.

But here is the cold reality that most drivers in 2026 don’t realize until their renewal letter arrives: Innocence does not mean free. When you follow the "standard route" of calling your own insurer, you trigger a chain reaction of administrative costs, excess fees, and risk profiling that can punish your wallet just as hard as the at-fault driver.

According to recent data from the Association of British Insurers (ABI), the average price of car insurance has seen volatility due to rising repair costs and parts shortages. But the real stinger? Industry analysis suggests that drivers with a non-fault claim on their record can still see their premiums hike by up to 15-20% at renewal.

Table of Contents

Does Non-Fault Accident Affect Insurance? (The Direct Answer)

Yes, unfortunately, it often does. Even if the accident was 100% the other driver's mistake, reporting it to your own insurer opens a file on your history. Insurers use "Risk Profiling algorithms" which statistically view drivers involved in any accident—regardless of blame—as having a higher likelihood of being in another incident soon. This can result in your No Claims Bonus (NCB) being temporarily frozen or your base premium rising due to perceived "risk exposure."

The "Non-Fault" Penalty Explained: Why Premiums Rise for Victims

To understand why this happens, we have to look at insurance not as a justice system, but as a statistics game.

It’s Not Blame, It’s Statistics

Insurers operate on risk data. When you report an accident, even a non-fault one, you are statistically flagged. The logic is harsh: perhaps you drive on dangerous roads, or you park in a high-risk area, or you drive at peak "accident-prone" hours.

While you are legally innocent, the algorithm sees you as "accident-adjacent." In 2026, where insurers are tightening their belts due to the high cost of electric vehicle (EV) repairs, they are quicker than ever to price this risk into your renewal quote.

The "Open Claim" Danger

When you call your insurer to handle a non-fault claim, they open a file. Until they successfully recover 100% of the costs from the other driver's insurer, that file remains "Open."

- The Freeze: While a claim is open, your No Claims Bonus (NCB) is often "stepped back" or frozen.

- The Timing: If your policy renewal comes up while the insurers are still arguing (which can take months), you will have to pay the higher premium. You might get a refund later, but you are out of pocket now.

Key Insight: You are lending your insurer money (via higher premiums and excess) to fix a problem someone else caused.

The Loophole: Independent Claim Coordination

There is a better way. It is called Independent Claim Coordination, and it is the loophole that savvy drivers have been using to protect their premiums and sanity.

Accident Management Company vs Insurance

Instead of becoming a "claimant" on your own policy, you can use a service like Accident Assist Network. We act as a coordinator.

We verify the accident was not your fault, and then we direct the claim straight to the at-fault driver's insurance company.

- Bypassing Your Policy: Because the claim is directed elsewhere, your insurer doesn't have to pay out a penny. They are notified (for information only), which helps keep your risk profile cleaner.

- No Excess: Since you aren't claiming on your policy, there is no excess to pay.

- Manufacturer-Standard Repairs: We ensure your vehicle goes to a reputable specialist, not just the cheapest garage in the insurer's network. Read more about our Vehicle Repairs standards here.

Your Legal Right to "Like-for-Like" Mobility

Under English law (specifically Tort Law), if you are the victim of a non-fault accident, you are entitled to be put back in the position you were in before the crash.

This means you are entitled to a credit hire agreement explained simply: You get a replacement vehicle that matches yours (size, prestige, and function) while yours is off the road. The cost is recovered directly from the at-fault party's insurer.

If you drive a BMW, you get a BMW. If you drive a London Black Cab, you get a licensed taxi replacement. You don't have to settle for less.

For London’s Pros: Taxi & PCO Drivers

If you drive for a living, your vehicle isn't just a car; it's your office and your paycheck.

We know that for London Taxi Drivers and private hire drivers, "downtime" is the enemy. Standard insurers often struggle to source PCO-licensed vehicles quickly. This leaves you sitting at home while your bills pile up.

At Accident Assist Network, we specialize in keeping you moving. We can arrange a fully plated, ready-to-work vehicle (including LEVC electric taxis and Uber-ready hybrids) delivered to you within 24 hours.

- Don't lose your income.

- Don't lose your badge standing.

- Don't pay storage fees.

We understand the unique pressures of the trade. Check out our dedicated help for London Taxi Drivers to see how we keep the meter running.

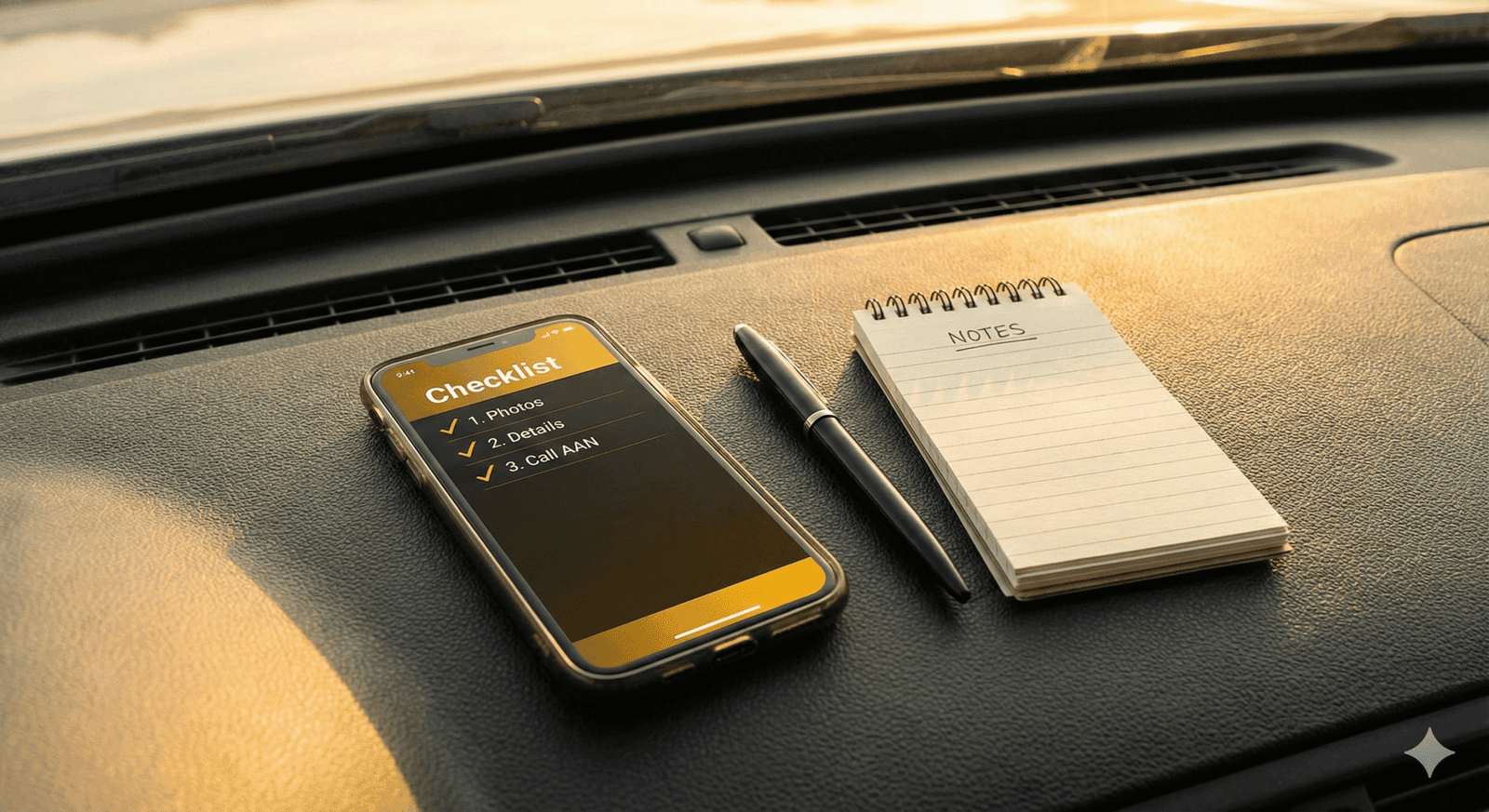

Your Post-Accident Survival Guide (5 Steps)

If the worst happens, panic is natural. But keeping a cool head can save you thousands. Here is your immediate action plan.

- Stop & Secure: Stop immediately. Turn on hazards. Ensure everyone is safe.

- Snap the Scene: Take photos of everything. The damage, the road layout, the other driver's number plate, and the weather conditions.

- Silence is Golden: Be polite, but do not admit liability. Do not say "Sorry, I didn't see you." Just exchange details.

- Witness Hunt: Get names and phone numbers of anyone who saw what happened. Independent witnesses are gold dust for proving non-fault status.

- Select Your Partner: Before you call your insurer (who might record it as a claim immediately), Call a Trustworthy Friend.

Calling Accident Assist Network first allows us to triage the situation. We can advise if the accident qualifies as non-fault and arrange Immediate Recovery to get you and your car to safety.

Conclusion: Don't Face the System Alone

The "2026 Insurance Trap" is real. The combination of rising repair costs, algorithmic risk profiling, and administrative hurdles means that innocent drivers are often the ones footing the bill.

But you have a choice. You don't have to accept the "Standard Route" of high excess, lost bonuses, and tiny courtesy cars. You can choose the independent route—the route that puts you first, not the insurance company's bottom line.

Whether you need a replacement taxi, help in Romanian, or just someone to handle the headache, we are here.

"Had an accident? Call a trustworthy friend."

Service Note & Mandatory Disclaimer

Accident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If the at-fault insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Please read every document thoroughly and, if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.

Need practical help in England?

Or Visit Contact Us

Engagement: Have Your Say

Poll: In the past, have you seen your insurance premium go up after an accident that wasn't your fault?

- [ ] Yes, it jumped significantly.

- [ ] No, it stayed the same.

- [ ] I'm not sure / I didn't check.

Frequently Asked Questions (FAQs)

Q1: How much does a non-fault claim affect my insurance?

Industry data suggests premiums can rise by 10% to 20% after a non-fault claim. This is because insurers view the incident as an indicator of increased risk. Using an independent coordinator can help mitigate this by handling the claim directly with the at-fault party.

Q2: Can I claim car insurance excess back?

If you use your own insurer, you must pay the excess first and claim it back later, which can take months. If you use Accident Assist Network, you do not pay any excess upfront because we claim directly from the at-fault driver's insurance.

Q3: What is a credit hire agreement explained simply?

A credit hire agreement allows you to hire a replacement vehicle while yours is being repaired, without paying upfront. The cost is recovered from the at-fault driver's insurer. It is the legal mechanism that allows us to provide "like-for-like" vehicles.

Q4: Do I have to use my insurer's recommended repairer?

No. You have the legal right to choose who repairs your vehicle. Insurer networks often focus on speed and cost-cutting. Independent networks prioritize Manufacturer-Standard Repairs to ensure your car's safety and value are maintained.

Q5: Is Accident Assist Network better than insurance?

For non-fault accidents, independent coordination often provides a superior service: no excess, better replacement vehicles, and protection of your NCB. However, for at-fault accidents, you must use your comprehensive insurance policy.