What should I do after a non-fault EV accident in London if my insurer wants to write it off?

If you've had a non-fault EV accident in London or across England, we coordinate practical vehicle help. This is for drivers needing recovery, an independent damage assessment, manufacturer-standard repairs, or a like-for-like EV replacement, including ULEZ-compliant taxis. We aim to deliver a replacement hire vehicle within 24 hours. There are no upfront costs; our small service fee is only deducted after the at-fault insurer settles your claim. Start by calling our 24/7 hotline or messaging us on WhatsApp for immediate support.

Q: How fast can I get a replacement EV?

A: We aim to deliver a like-for-like replacement EV, including licensed taxis, within 24 hours of starting your non-fault claim.

Q: Do I have to pay for this service?

A: There are no upfront costs. Our small, pre-agreed service fee is only deducted after the at-fault insurer has paid out the settlement for your vehicle damage claim.

Q: Is this service available for my PCO (taxi) licence?

A: Yes, our network provides like-for-like replacement vehicles that are fully ULEZ-compliant and licensed for PCO (TfL) use.

Had a Non-Fault EV Accident? Why Your Car Might Be Written Off (And What to Do)

The sound of crunching metal is awful. But for an electric vehicle (EV) owner, the real shock often comes days later. You've had a minor, non-fault accident. You're safe, and the damage looks superficial—a dented bumper, a cracked headlight. Your stress, however, is just beginning.

Instead of scheduling a simple repair, your insurer is using confusing terms. They mention "specialist assessment delays," "battery integrity checks," and the terrifying phrase "potential total loss." For a small dent? It feels unjust, illogical, and deeply unfair.

You are not alone. This is the 2025 "EV write-off trap" that thousands of UK drivers are falling into. This isn't just a feeling; the data proves it. Handling an EV Accident claim is now a major financial risk, with recent reports showing the average EV insurance premium has soared to £1,344—nearly double that of traditional petrol cars.

Direct Answer (AEO Snippet): An EV Accident claim often leads to a write-off for minor damage because of three key factors:

- The high cost of "smart" parts like sensor-filled bumpers.

- The risk to the structural battery pack, where a small knock can compromise the entire unit.

- A nationwide shortage of high-voltage (HV) certified technicians.

This article explains why this is happening and what practical steps you must take to protect your vehicle and your finances.

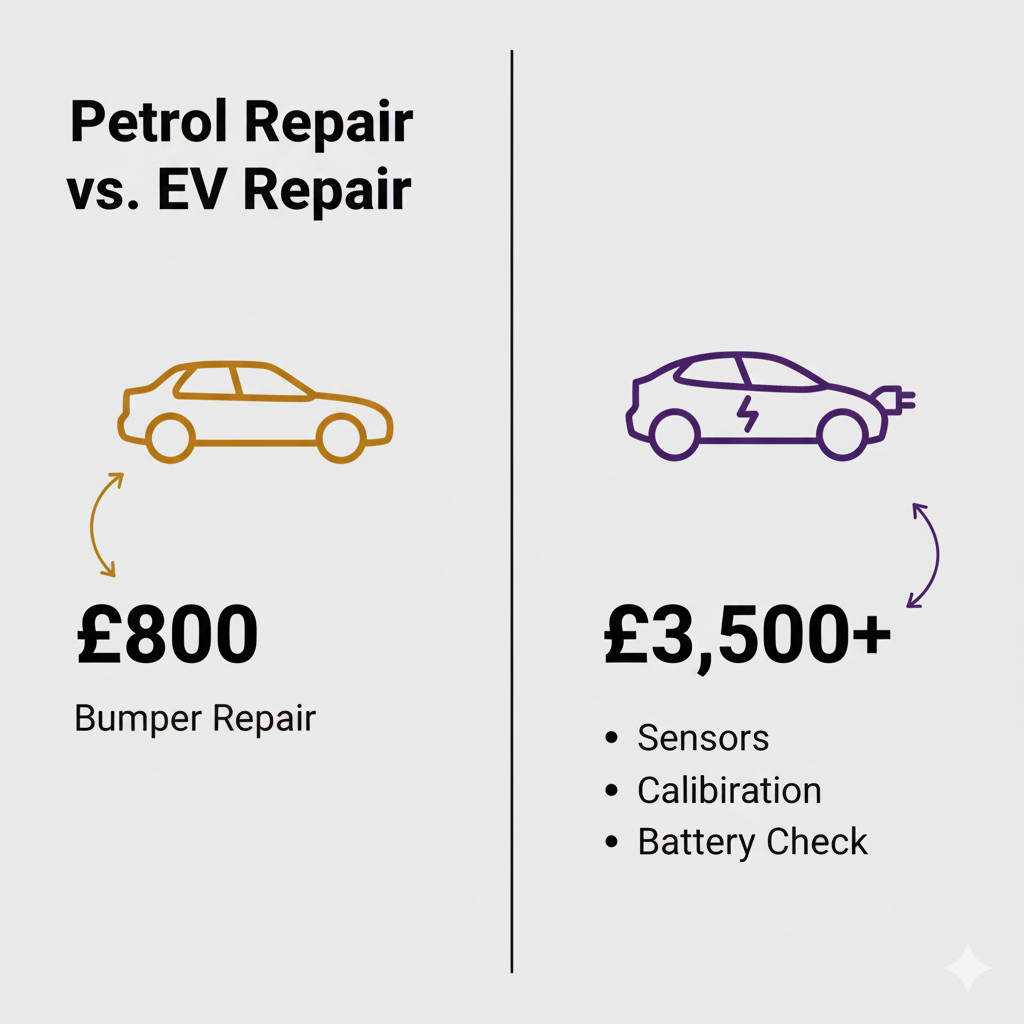

| Damaged Part | Typical Petrol Car (e.g., Ford Focus) | Equivalent EV (e.g., VW ID.3) | Why the Difference? |

|---|---|---|---|

| Rear Bumper (Dent) | £600 - £900 | £2,500 - £4,000+ | EV bumpers are packed with proximity sensors, cameras, and radar (ADAS) that need specialist replacement and recalibration. |

| Side Panel (Scrape/Dent) | £800 - £1,200 | £4,000 - £15,000+ | On many EVs, the side sill is part of the structural "skateboard" chassis. A dent here can trigger an inspection or replacement of the entire battery pack. |

| Cracked Headlight | £250 | £1,500+ | Modern EV headlights are often "Matrix LED" units, which are complex and expensive sealed components. |

Table of Contents

Why a 'Minor' EV Bump Can Cost £20,000

The old rules of car repair no longer apply. With a petrol car, a mechanic could fix a dented panel or replace a bumper for a few hundred pounds. With an EV, that same minor impact involves a completely different, and far more expensive, set of problems.

The Structural Battery Pack Problem

In the past, a fuel tank was a separate, protected box. On most modern EVs, the battery pack isn't just a component—it's the floor of the car. This "skateboard" design is great for handling and space, but it's an insurance nightmare.

Even a minor hit to the sill (the panel under the door) or the car's underside (like hitting a high kerb or pothole) can create a microscopic fracture in the battery's sealed casing. This creates a risk of water ingress and, in rare cases, a thermal runaway fire.

Because the risk is so high and the technology is so new, many manufacturers forbid repair, demanding a full replacement. With a new battery pack costing £15,000 to £25,000, it's often more than the car's entire market value.

"Smart" Parts and Sensor Calibration Costs

That "simple" bumper on your EV is a high-tech command centre. It's packed with LiDAR, radar, cameras, and ultrasonic sensors that govern your car's Advanced Driver-Assistance Systems (ADAS).

When that bumper gets cracked in a non-fault accident, you can't just fix the plastic. The entire unit, and its expensive sensors, must be replaced. After installation, the system requires hours of specialist recalibration to ensure it's accurate. According to Thatcham Research, the UK's automotive risk intelligence experts, this complexity means EV repairs can cost 25% more and take 14% longer than their petrol counterparts.

The Nationwide Technician & Parts Shortage

Your local garage almost certainly cannot fix a structural EV. Repairing a high-voltage (HV) system is dangerous and requires specialist certification.

The Institute of the Motor Industry (IMI) has issued stark warnings about this "skills gap." Their latest 2025 forecast shows that while the number of qualified EV technicians is growing, it's lagging far behind demand, with a projected shortfall of over 25,000 technicians by 2035.

This shortage creates a massive bottleneck. Longer wait times for a specialist bay, combined with parts delays, mean your claim costs (including a hire car) spiral. For an insurer, it's often cheaper and faster to just write the car off.

| Problem | The Cause | The Consequence for Your Claim |

|---|---|---|

| 1. Structural Battery | The battery is the car's floor. A minor hit can compromise the whole pack. | Insurers default to a write-off to avoid the risk and cost of a £20,000 battery replacement. |

| 2. Complex "Smart" Parts | Bumpers and lights are full of expensive ADAS sensors. | A simple part replacement now costs thousands and requires specialist recalibration, inflating the repair bill. |

| 3. Skills & Parts Gap | A nationwide shortage of HV-certified technicians and parts. | Long delays and high labour costs make insurers favour a "total loss" decision over a complex, lengthy repair. |

The "Non-Fault" Fallacy: Why You Still Lose

This is the part that feels most unjust. "But it wasn't my fault!" you say. "The other driver admitted liability!"

Unfortunately, a "non-fault" status only protects your No Claims Bonus and means the at-fault insurer is paying the bill. It does not stop your EV Accident claim from being a write-off.

The "Economic Total Loss" Trap

An insurer's decision is not emotional; it's simple maths. They will declare your car an "economic total loss" if the cost of repair (plus parts, storage, and hire car) approaches or exceeds its "Pre-Accident Value" (PAV).

Because of the three problems we just discussed, your EV Accident claim hits that "total loss" threshold incredibly quickly. The insurer writes the car off, gives you a payout, and your finance agreement may still leave you owing thousands on a car you no longer even own.

The PCO Driver's Nightmare: No "Like-for-Like" Replacement

This "trap" becomes a financial catastrophe if you are a professional driver.

Imagine you are a London Taxi or PCO driver. You've invested in a ULEZ-compliant electric taxi to do your job. You are hit by another driver (100% non-fault). Your insurer happily provides their "standard courtesy car"—a 1.0-litre petrol hatchback.

This car is useless to you. It's not TfL-plated. You cannot use it for work.

You are now in a living nightmare. You are not at fault, but you are unable to earn a living. Every day the claim drags on, you are losing money, all because of an EV Accident claim that your insurer's network isn't equipped to handle.

Service Note & Mandatory Disclaimer

Accident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If the at-fault insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Please read every document thoroughly, and if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.

How to Take Back Control of Your Non-Fault EV Claim

If you are in this situation, you are not powerless. The key is to understand that your insurer's "total loss" decision is their preferred solution, not your only one. Here is how you take control of your EV Accident claim.

Step 1: Know Your Rights (Before You Call Your Insurer)

After a non-fault accident, you have the right to choose who repairs your vehicle. You are not legally obliged to use your insurer's "approved" garage, which may not be EV-certified. You also have the right to a "like-for-like" replacement vehicle from the at-fault party, not just the basic car your own insurer offers.

Step 2: Demand an Independent Damage Assessment

This is the most critical step. An insurer's default "write-off" is often a quick decision based on high-level estimates. You can challenge this.

A specialist accident coordinator, like Accident Assist Network, works for you, not the insurer. We can facilitate an independent damage assessment from an EV-certified specialist. Their goal is to see if a safe, manufacturer-standard repair is possible, rather than defaulting to a premature write-off. This gives you a true picture of the damage and a powerful second opinion.

Step 3: Secure a True "Like-for-Like" Replacement Vehicle

This is especially vital for professional drivers. You must not accept a "standard" hire car that stops you from working.

The at-fault insurer is liable for putting you back in the position you were in before the accident. This means a car of a similar size, standard, and specification—including an EV if that's what you drive.

Our network includes partners who can provide a true like-for-like replacement hire vehicle, including TfL-plated EVs for taxi drivers and vans for couriers. This single step can save your EV Accident claim from costing you your livelihood.

| Your Problem | Insurer's Default Path (The "Trap") | Your Rights (The "Solution") |

|---|---|---|

| "Minor" Damage | Declares an "Economic Total Loss" to avoid repair complexity and cost. | You have the right to an Independent Damage Assessment from an EV specialist. |

| Replacement Car | Offers a basic, small petrol "courtesy car" from their own fleet. | You are entitled to a Like-for-Like Replacement (e.g., another EV or a TfL-plated taxi) from the at-fault insurer. |

| The Process | You are stuck in their system, dealing with their assessors and garages. | You can use an Independent Coordinator (like us) to manage the entire process on your behalf. |

Your Next Steps: What to Do Right Now

A non-fault accident in your EV can feel like being punished for going green. The technology is new, the rules are confusing, and the risk of losing your car—or your livelihood—is terrifyingly real. You are right to be concerned about your EV Accident claim.

Service Note & Mandatory Disclaimer

Accident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If the at-fault insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Please read every document thoroughly, and if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.

But you are not powerless. The key is to remember your rights: the right to an independent assessment and the right to a true like-for-like replacement. If you've had a non-fault accident in England and feel trapped in this EV nightmare, "Had an accident? Call a trustworthy friend". We coordinate the practical help you need to challenge an unfair write-off and get back on the road.

We are happy to guide you in the language you feel most comfortable with.

Need practical help in England?

Or Visit https://accidentassistnetwork.co.uk/

Reader Poll:

What is your BIGGEST worry about an EV accident?

- ( ) High repair costs.

- ( ) Insurers writing it off for minor damage.

- ( ) Not being able to get a like-for-like EV hire car.

- ( ) Finding a specialist EV repair garage.

Frequently Asked Questions (FAQs)

1. What makes an EV Accident claim different from a petrol car claim?

The main difference is cost and complexity. An EV Accident claim involves expensive "smart" parts (sensors, cameras) and, most importantly, the risk to the structural battery pack. A minor bump that's a simple fix on a petrol car can threaten the entire battery pack on an EV, leading to a much higher chance of a total loss.

2. Can I get a like-for-like EV replacement car after a non-fault accident?

Yes. If the accident was not your fault, the at-fault party's insurer is legally responsible for putting you back in the position you were in. This includes providing a like-for-like replacement vehicle. If you drive an EV, you are entitled to an EV. If you drive a licensed taxi, you are entitled to a licensed taxi.

3. Will an EV Accident claim mean my car is automatically written off?

No, not automatically. However, the risk is much higher than with a petrol car. Insurers will write it off if they decide the cost of a specialist repair (including parts, labour, and potential battery replacement) is more than the car's current value. This is why getting an independent assessment is so important.

4. Why does my insurer want to write off my EV for minor damage?

It's a financial decision for them. There is a shortage of EV-certified technicians, parts are expensive, and there is a high-risk liability around battery safety. For many insurers, it is cheaper, faster, and safer for them to declare the car a "total loss," pay you out, and sell the car for salvage.

5. Can I challenge my insurer's decision on my EV Accident claim?

Yes. You can and should get a second opinion. An independent coordinator can help you arrange an assessment from a certified EV specialist garage to determine if a safe, manufacturer-standard repair is a viable option, even if your insurer's preferred garage says it isn't.

6. What should I do first after a non-fault EV accident?

First, ensure everyone is safe and report the incident to the police. Gather the other driver's details and take photos. Then, before you commit to your insurer's process, call an independent accident coordinator. They can protect your interests from the start, arranging for recovery and a like-for-like hire car without you having to battle your insurer.

7. Does Accident Assist Network handle the financial or personal injury part of a claim?

No. Accident Assist Network is not authorised or regulated by the FCA. Our role is one of practical facilitation for vehicle damage only. We co-ordinate the non-fault vehicle recovery, storage, replacement hire, and repairs. We do not handle any personal injury aspects, nor do we provide any financial or legal advice.