Do I Have to Pay the Excess if the Accident Wasn’t My Fault?

UK drivers ask: do i have to pay excess if not my fault? Here’s the practical answer—and the fastest ways to get it back.

You did nothing wrong—so why are you being told to pay? If you’ve just had a non-fault crash, the word “excess” lands like another punch: it feels unfair, your car’s off the road, and you’re worrying about work, kids, and cash-flow—all at once.

Let’s fix the confusion, fast. This guide shows when you might pay an excess upfront, how to reclaim it, and which routes can help you avoid paying upfront in the first place. We keep it practical, step-by-step, and rooted in trusted UK sources.

We reference guidance from Citizens Advice, MoneyHelper, the Financial Ombudsman Service, and independent reporting.

Quick Answer

If you claim on your own policy, you often pay the excess up front and then claim it back from the at-fault insurer once liability is accepted. Some routes (direct third-party claims or certain credit-hire/repair arrangements) can avoid paying upfront, depending on liability clarity and policy rules. See Citizens Advice and Financial Ombudsman Service.

Primary keyphrase: do i have to pay excess if not my fault

What “Excess” Really Means (in Plain English)

Excess is the first part of a claim you agreed to pay. In UK insurance, compulsory excess is set by the insurer; voluntary excess is what you add to reduce premiums. If a claim is made on your policy, the insurer deducts your total excess from the payout or collects it at repair. See MoneyHelper and the ABI glossary.

So, do i have to pay excess if not my fault? It depends on the route you choose: if you use your own policy to move repairs quickly, you may pay first and reclaim later; direct third-party or AMC routes might avoid upfront payment.

Mini-glossary

- Non-fault: the other driver is responsible (or their insurer pays the losses).

- Liability accepted: the other insurer confirms their driver caused it; your outlay (like excess) is recoverable.

- Third-party capture: when the at-fault insurer contacts you directly to settle. See Citizens Advice guidance.

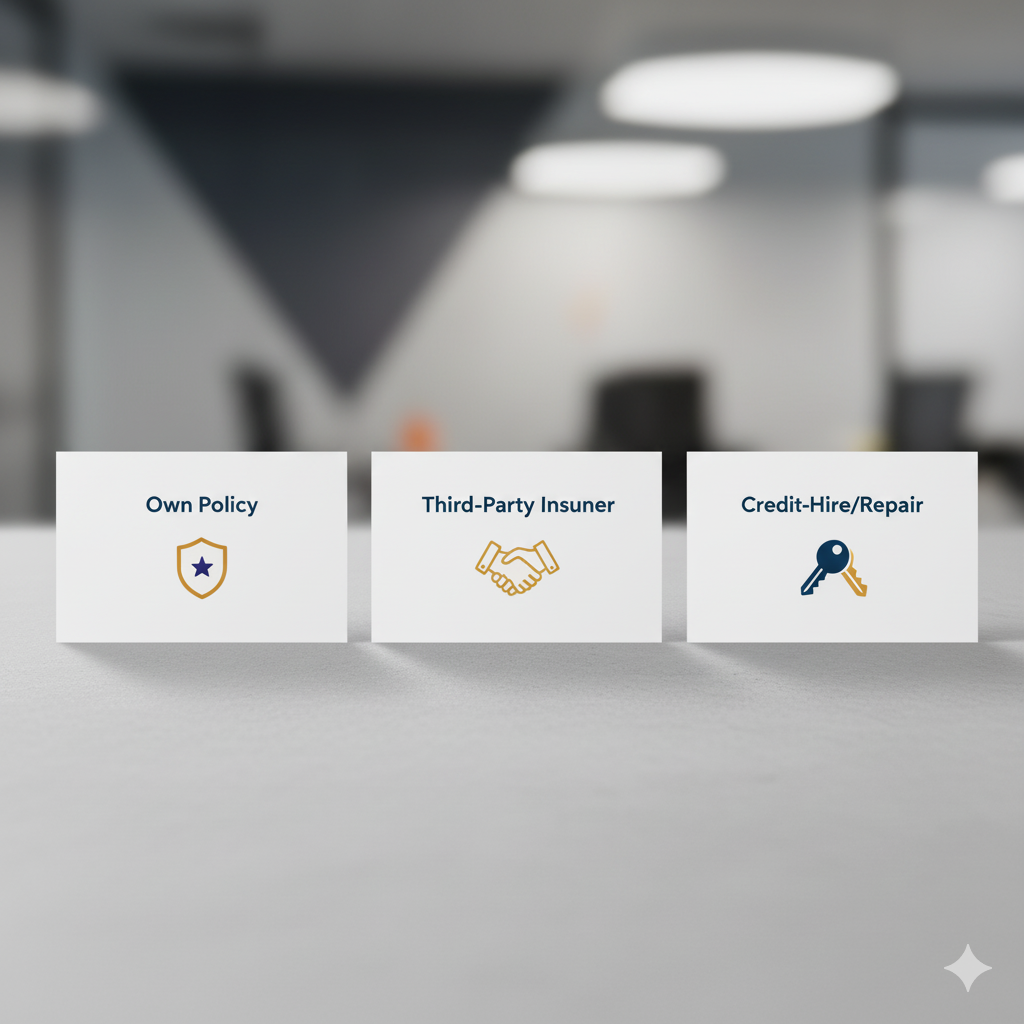

Your Three Main Routes (Speed vs Cash-Flow vs Admin)

1) Claim on your own policy — fast repairs, pay now, reclaim later

This is often the quickest way to get repairs moving and secure a courtesy car or approved hire. The trade-off: you’ll typically pay your excess up front and then reclaim it once the at-fault insurer accepts liability. See Citizens Advice and MoneyHelper.

Use-case: you need speed and certainty, and have clear evidence to support recovery of costs.

2) Direct claim to the third-party insurer — possible excess waiver

Sometimes the other insurer will handle your claim directly. This can mean no upfront excess—but responsiveness varies, so get everything in writing and check repair standards. See Citizens Advice on direct approaches.

Use-case: liability looks obvious (e.g. parked car hit) and the other insurer is responsive.

3) Credit-hire / credit-repair via an Accident Management Company — no upfront when liability clear

AMCs can arrange like-for-like mobility and repairs without upfront costs when the case appears clearly non-fault. If liability later flips, you could face hire or storage charges—read contracts carefully. See the consumer pages at Financial Ombudsman Service.

Use-case: you must keep earning (taxi, van, delivery bike) and have strong evidence the other driver is at fault.

How to Reclaim Your Excess — Fast (Plain-English Steps)

- Gather evidence early: photos, dashcam, witness details, police reference, repair invoices, and correspondence. Strong evidence speeds up liability acceptance and recovery. See Citizens Advice.

- Know who chases what: If you claimed on your policy, your insurer (or panel solicitor) typically pursues the at-fault insurer for your outlay (including excess). If they don’t, ask how to reclaim directly from the other insurer.

- Keep a tidy paper trail: send copies not originals; save emails as PDFs; diarise dates. Clear documentation shortens delays—common in today’s claims environment (see Financial Times).

- Escalate if stuck: use the insurer's complaints route and, if unresolved, go to the Financial Ombudsman Service.

Many readers search do i have to pay excess if not my fault because they already paid; this section helps you recover it quickly.

If Liability Is Disputed or Delayed

Stay mobile and protect your position. Proceed with the route that keeps you working, but keep evidence tight and communications in writing. If you paid your excess, continue the recovery process while liability is investigated. Use the formal complaints path before contacting the Ombudsman — first complain in writing to the insurer and allow time to respond, then escalate to the Financial Ombudsman Service if needed.

Mind your NCD — ensure your policy records are corrected when the case is confirmed non-fault.

Credit Hire & Repair: When It Helps — and What to Watch

When it helps: if you’re clearly non-fault and need like-for-like mobility (taxi-plated, correct payload van, or delivery bike), credit-hire can keep you earning without upfront payment while repairs are arranged. See FOS guidance.

Risks: if liability is later disputed or hire is unreasonable in rate/duration, you could be exposed to charges under your contract with the AMC — read every clause and keep hire reasonable. See reporting in the Financial Times.

Safeguards: get written indicators of fault, keep hire duration realistic, and store receipts, photos, and repair updates.

Service Note & Mandatory Disclaimer (read carefully)

Accident Assist Network assists after a non-fault accident by coordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of specialist companies across England. We are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If the at-fault insurer delays or disputes payment you may become liable for credit services or other charges under your contract. Please read every document thoroughly and, if anything is unclear, ask us or an independent adviser before signing.

Need practical help in England?

Call: 020 4577 1120 · WhatsApp: 07585 300 600

Conclusion

You’re not powerless. Now you know why an excess is sometimes taken upfront, how to get it back, and when there are routes to avoid paying upfront altogether. Short, confident steps — clear evidence, tidy records, and the right claim route — beat endless worry.

Had a non-fault accident and need practical help? Visit accidentassistnetwork.co.uk

Poll — Which route would you choose today?

Frequently Asked Questions

Do I have to pay excess if not my fault—always?

Not always. If you claim on your policy you usually pay first and reclaim later when the other insurer accepts liability. Direct third-party claims or certain credit-hire/repair paths might avoid upfront payment. See Citizens Advice and FOS.

How do I claim my excess back?

Keep evidence tidy (photos, witness details, invoices). Ask your insurer how they are recovering your outlays; if needed, submit a reclaim to the at-fault insurer. If stalled, use insurer complaints path and the Ombudsman. See Citizens Advice.

Can I avoid paying the excess upfront?

Possibly — direct third-party claims or credit-hire/repair may avoid upfront cost when liability is clear. Always read contracts. See Citizens Advice and FOS.

Will this affect my no-claims discount (NCD)?

If the case is confirmed non-fault and records are corrected, your NCD should not be impacted. Get corrections in writing and check your renewal documents. See FOS.

What if an insurer isn’t responding or keeps delaying?

Follow the complaints process and escalate to the Ombudsman if unresolved. The Ombudsman is free and can issue binding decisions. See Citizens Advice.

Is third-party “capture” legit?

Yes — being approached directly by the other driver’s insurer is legal. Ensure any offer covers like-for-like repairs and mobility before agreeing. See Citizens Advice.

Why are claims slower and more expensive now?

Modern vehicles are more complex; parts can be delayed and some insurers face service pressures. Strong evidence and tidy paperwork help reduce delays. See Financial Times.