let’s name the worry

A bump on a busy road can leave you staring at your phone, asking: Will this be a fault accident claim or a non fault accident claim—and what does that change for me? You’re worried about work, your no claims discount, and how quickly a like-for-like car or bike arrives.

we keep it human and practical

This guide breaks the difference between fault and non fault accident claims into plain steps. We’ll show how evidence changes outcomes, what happens to your excess and NCD, and how no fault accident claims can unlock credit-hire like-for-like vehicles when appropriate—without legal jargon or scare tactics.

context that matters

Road incidents are common and costly. UK motor insurers paid a record £11.7bn in 2024, reflecting heavier repair costs and claim volumes (Association of British Insurers). See the ABI’s analysis here. ABI

Great Britain also reports substantial annual road casualties, reminding us why clear guidance matters—see the Department for Transport’s 2024 statistics here.

Direct answer

In the UK, the difference between fault and non fault accident claims is about cost recovery. A non fault accident claim means your insurer (or third-party route) can recover 100% of costs from the at-fault driver’s insurer. A fault accident claim is recorded when you caused it or costs cannot be fully recovered (e.g., unknown third party, animal strike). Sources: FOS, Allianz.

What a non fault accident claim looks like in real life

Think “recovery.” A non fault accident claim relies on proving the other driver’s liability and recovering all costs from their insurer. When recovery succeeds, your NCD usually isn’t reduced, and any excess you paid can often be reclaimed once settlement clears. See Aviva and Citizens Advice.

Why it matters: For working drivers—PHV/taxi, couriers, riders—no fault accident claims can support like-for-like credit-hire cars or bikes (where appropriate) while your vehicle is off the road.

Common mistake: Confusing “I didn’t cause it” with non-fault automatically. If evidence is weak or the third party disappears, the insurer may record a fault accident claim until/unless recovery happens (see FOS guidance).

What a fault accident claim means (even if you didn’t “cause” it)

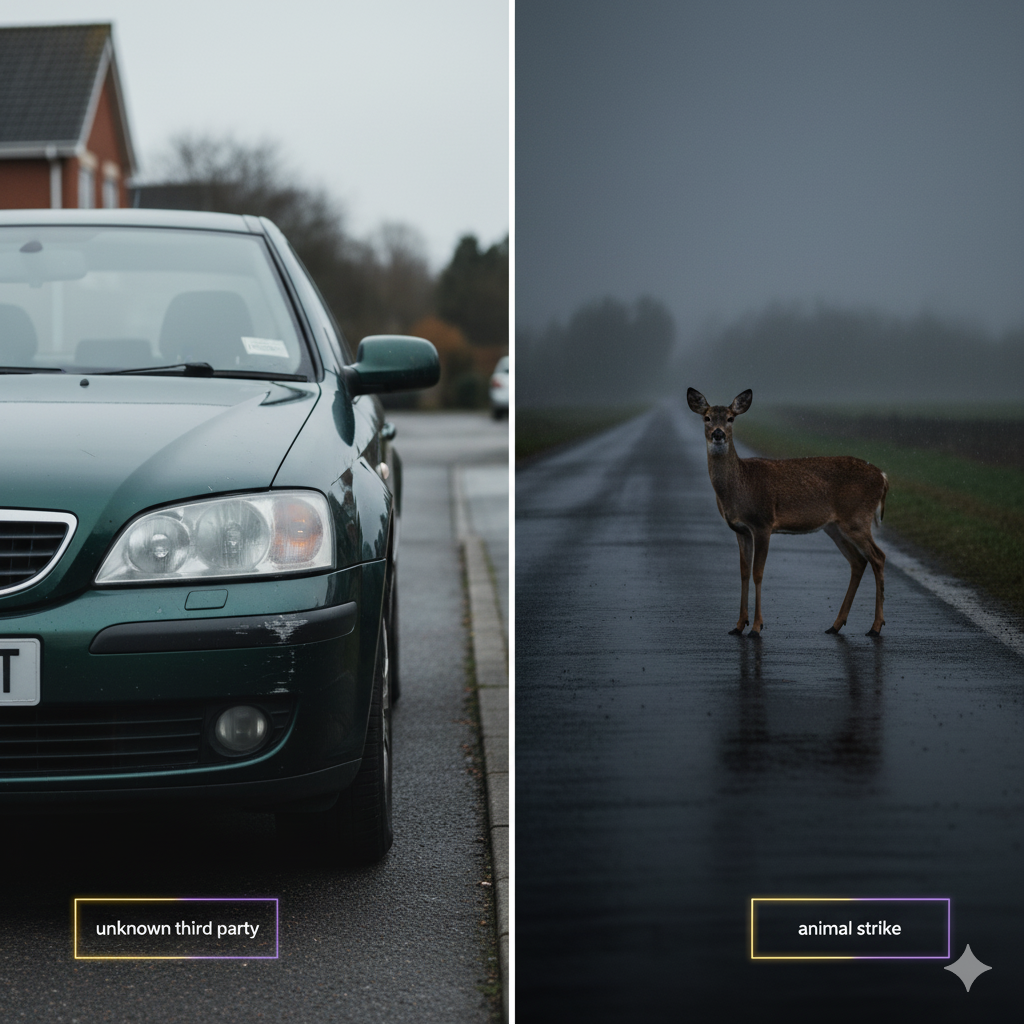

When it’s recorded as “fault.” A fault accident claim is noted if you caused the incident or if your insurer cannot recover costs—think hit-and-run, unknown driver, animal strike, or shared liability. The Financial Ombudsman explains how this affects your record and NCD—see their page here.

NCD impact and timeframes. With a fault accident claim, unprotected NCD typically steps back. Aviva outlines NCD step-backs and policy variations here.

Can a claim “flip” later? Yes. If new evidence appears (e.g., CCTV), a recorded fault accident claim can be re-assessed after successful recovery. The principle—recovery drives the label—is echoed by Allianz.

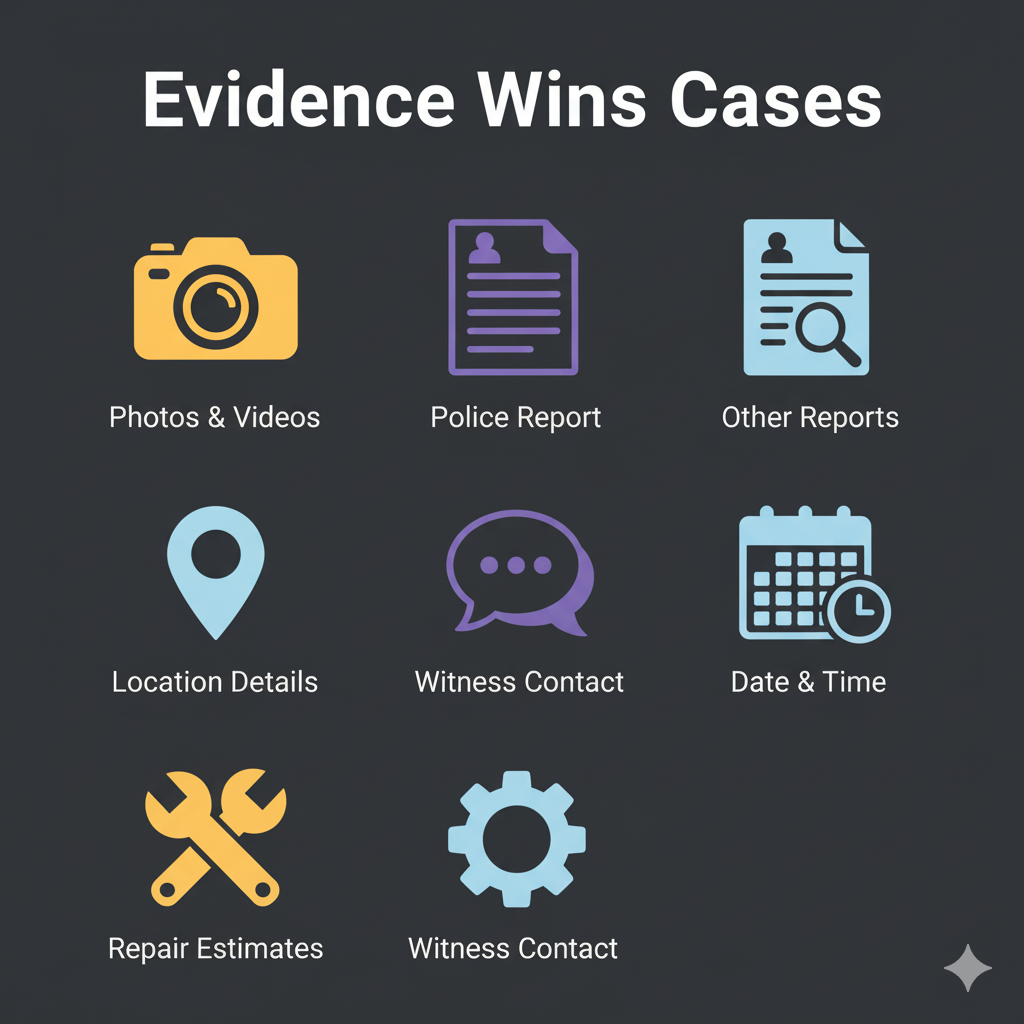

The 7-item evidence checklist that decides outcomes

If you want the difference between fault and non fault accident claims to land in your favour, evidence is everything. Capture, store, and share the right items quickly.

Photos & video: wide shots, close-ups, and road layout.

Dashcam clip: back up footage securely off-device.

Witness details: names, phone, quick notes.

Third-party details: reg, insurer, policy number if available.

Location & time: note signage, lane markings, lights.

Police reference: if applicable.

Scene notes: weather, traffic, anything unusual.

See practical claiming steps from Citizens Advice.

Avoid apologising or admitting blame at the scene; keep statements factual and polite. (General consumer guidance and ombudsman case patterns support this approach; start with FOS overview.)

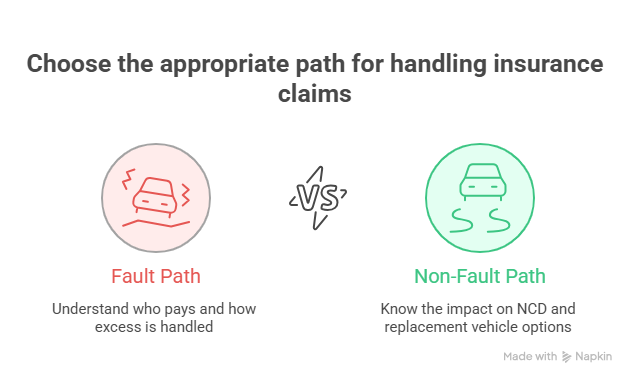

Excess, NCD and your replacement vehicle: what changes under each path

Excess (short and clear). Even on a non fault accident claim, you might pay your policy excess first and claim it back after recovery—see Citizens Advice.

NCD (what usually happens). With no fault accident claims, if recovery is 100%, your NCD is typically preserved; a fault accident claim usually steps NCD back if it’s not protected—see Aviva and the FOS. Replacement route (courtesy vs credit-hire).

Courtesy: usually basic spec, policy/repairer-dependent, limited availability.

Credit-hire: like-for-like in no fault accident claims, costs aimed at the at-fault insurer (subject to case specifics and industry practice). For a plain-English grounding, start with Allianz’s consumer explainer.

Quick scenarios (so you can self-route with confidence)

Rear-end at lights (PHV/taxi). Strong evidence + third-party details → typically a non fault accident claim once liability is admitted; you may reclaim excess after settlement; NCD preserved per recovery. See principles in FOS overview.

Car-park scrape; no note left. Unknown third party → insurer cannot recover → recorded as a fault accident claim for now; if CCTV later identifies the driver and recovery succeeds, the label can change. Cross-check the idea with Allianz explainer.

Animal strike on an A-road (van). No one to recover from → commonly recorded as fault; check policy for courtesy-car provisions. The difference between fault and non fault accident claims is who pays and whether your insurer can recover. See FOS. Disputed sideswipe (bike). If you collect dashcam, witnesses and CCTV, a fault accident claim can become a non fault accident claim after successful recovery—aligns with Allian z/Aviva consumer pages (Allianz, Aviva).

Service note & Mandatory Disclaimer (place above first CTA)

Accident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If the at-fault insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Please read every document thoroughly and, if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.”

Need practical help in England?

Call: 020 4577 1120 · WhatsApp: 07585 300 600

When to ask for help (and what a good call sounds like)

If you’re stuck between a fault accident claim and a non fault accident claim, say exactly what evidence you have, where it’s stored, and if there are witnesses or CCTV you can access.

Ask clear questions: “Do I pay the excess now?”, “What happens to my NCD if recovery is partial?”, “Is a like-for-like vehicle available under no fault accident claims for my work vehicle?”

Keep timelines realistic. Even with a strong non fault accident claim, recovery can take time. ABI’s payout trends show high volumes—see the latest context here.

Conclusion

empathy + solutions

Crashes are noisy and stressful. But the difference between fault and non fault accident claims is simpler than it feels: if your insurer can recover all costs, it’s a non fault accident claim; if they can’t, it’s a fault accident claim for recording. Your job is to collect evidence early so the label—and your outcomes—are fair.

recap + soft next step

To protect your NCD and reclaim excess, build your file now: photos, dashcam, witnesses, police ref. If you want friendly, plain-English coordination after a non fault accident claim, visit Accident Assist Network for recovery, storage, reputable repairs and like-for-like hire options in England.

quick engagement

Would a one-page decision tree help you decide if your case is likely a non fault accident claim or a fault accident claim? Vote Yes/No and tell us which scenario is hardest to judge.

FAQS

Often yes—upfront—then you may reclaim it after the other insurer pays out in full. See Citizens Advice.

Usually yes if it’s not protected, because a fault accident claim often steps back your NCD at renewal. See Aviva’s NCD notes.

Not always. Courtesy cars are policy/repairer benefits and can be basic. In some no fault accident claims, a like-for-like credit-hire route may be appropriate. For consumer-friendly context, see Allianz.

Evidence: dashcam, witnesses, CCTV, police refs, and consistent statements. If recovery is partial or impossible, it’s recorded as a fault accident claim; full recovery supports a non fault accident claim. See FOS overview.