Can I choose my own repairer after an accident?

Yes—usually you can choose your own repairer after a non-fault accident, provided your choice is reasonable on cost and method. Insurers must handle claims promptly and fairly under the FCA’s rules, though they may incentivise approved repairers. Keep quotes, timelines and communications in writing to protect your position. See the FCA Handbook (ICOBS 8.1)

Can I choose my own repairer after an accident in London & across England?

If your crash was non-fault and vehicle-damage only, you can choose your own repairer as long as costs and methods are reasonable. We coordinate recovery, secure storage, reputable repairs and like-for-like replacement—typically within 24 hours (12h in major cities where stock allows). There’s no upfront cost; our pre-agreed service fee is deducted after the at-fault insurer settles. To start now, call 020 4577 1120 or WhatsApp 07585 300 600.

How fast can I get a replacement?

We aim to deliver within 24 hours; 12h in major cities where stock allows.

Do I pay anything upfront?

No upfront cost; the fee is deducted after the at-fault insurer’s settlement.

Are vehicles work-ready and compliant?

Yes—like-for-like options (incl. taxi-plated/PCO, vans, bikes) are supplied road-legal and ready to work.

You, right now

Your car’s off the road, the insurer’s “approved” repairer says three weeks, and someone mentions a “non-approved repairer” excess. You’re not trying to argue—you just want safe repairs, a fair process, and a way to stay mobile. If you’re a taxi/PHV driver, downtime means lost income. If you’re a parent, it means missed plans.

Good news with boundaries

In the UK, you generally can choose your own repairer after a non-fault crash. The key is evidence: like-for-like quotes, a clear repair method, and a tidy timeline. If delays are the insurer’s fault, you can politely ask for help with excess or mobility. The fairness test matters more than the loudest voice.

Why this matters now (context + sources)

Motor claims paid reached £11.7bn in 2024—a record—so repair costs, capacity and courtesy cars are under pressure. That’s why networks push for control and why documentation protects you. Source: Association of British Insurers (ABI) news, 14 Feb 2025. Claims must still be handled promptly and fairly: see FCA ICOBS 8.1. For practical dispute outcomes, check the Financial Ombudsman Service motor insurance pages.

How the system works (plain-English map)

The moving parts

Your insurer (own-policy route): Must handle claims promptly and fairly, give reasonable guidance, and avoid unfair barriers. Reference: FCA ICOBS 8.1.

At-fault insurer (third-party assistance): Might offer repair/hire via its network to control costs; you’re not obliged to accept. Reference: ABI Third-Party Assistance claimant guide (PDF).

Credit hire/repair providers: Helpful when you’re off-road, but understand risks and who you can complain to. Read the FOS guidance on credit hire/credit repair.

Where your choice fits

You can usually proceed with your own repairer after a non-fault accident as long as your costs and method are reasonable and the insurer can authorise the work. Some policies incentivise network repairers with perks (e.g., easier courtesy car, sometimes a waived excess). Reasonableness and clarity win arguments.

Two truths to hold at once

Insurers have cost/quality controls in a high-inflation repair market—this isn’t always “bad faith”. See ABI context.

You still have agency. If you can show like-for-like work at a comparable or lower total cost with a sound repair method, choosing your own garage is a realistic path. The FOS repairs page explains how they look at fairness.

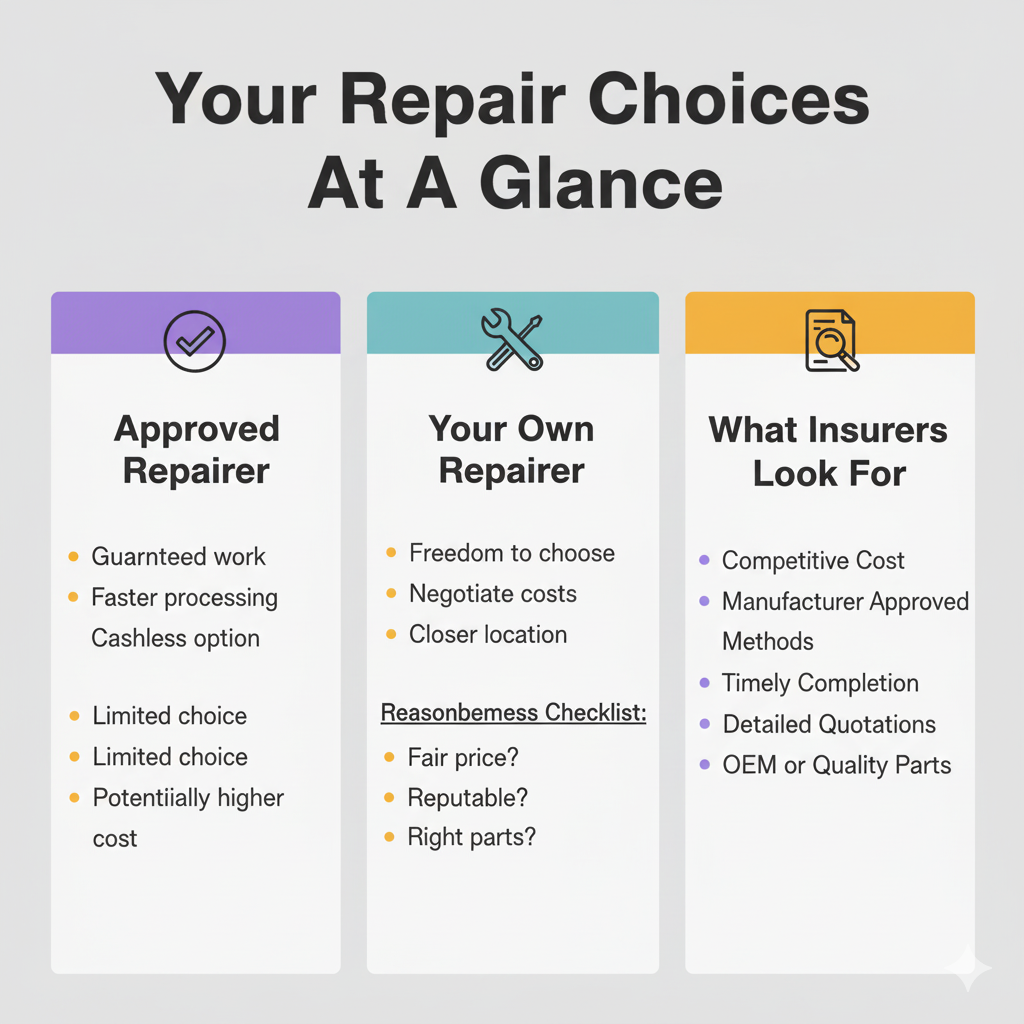

Approved vs your own repairer — choosing without regret

When an approved repairer might suit you

Faster authorisation: network rates/methods are pre-agreed.

One-stop rectification: if something goes wrong, the insurer’s route to a fix can be smoother.

Perks: sometimes easier courtesy car access or an excess incentive (varies by policy—read yours).

When your own repairer may be better

Availability now: your trusted garage can often book you sooner.

Communication/quality: you value direct updates and known workmanship.

Price parity or better: if your garage quotes like-for-like parts/method and a comparable or lower price, that’s powerful evidence.

Realistic trade-offs & how to manage them

Non-approved repairer excess: Some policies add one. If insurer-side delays caused your predicament, you can politely request a waiver or goodwill. Keep a dated log. The FOS routinely weighs timelines and communication quality—see their vehicle repairs guidance.

Courtesy car availability: Often easier via networks. If you need like-for-like for work, consider options but keep costs reasonable; read the FOS credit hire guidance.

Method disputes: Be ready to reference a recognised procedure (manufacturer repair portal or equivalent) and ask the engineer to state any objections in writing.

Proving your choice is reasonable (the 5-step method)

Step 1 — Photograph everything

Take clear photos from multiple angles, including VIN, wheel alignment areas and any panel gaps. Save dashcam/CCTV clips with timestamps. Put it all in one folder named with the incident date.

Step 2 — Get two like-for-like quotes

Ask both garages for: labour rate, paint/booth time, parts (OEM or OE-equivalent), lead time, and a short method note (e.g., manufacturer reference). Comparable detail shows reasonableness.

Step 3 — Send neatly, ask clearly

Email your handler with both quotes and photos. State why you prefer your own repairer (sooner start, comparable/lower price, recognised method). Request authorisation and ask for specific objections in writing if they disagree. Keep it polite and factual.

Step 4 — Keep a one-page timeline

Log dates: claim notification, inspection booked, inspection done, parts ETA, authorisation given. If insurer-side delays create loss of use, ask for help (e.g., non-approved excess waiver or mobility). The promptness and fairness duty is clear in ICOBS 8.1.

Step 5 — Sanity-check credit hire/repair

If you go off-policy into credit hire/repair, read every clause. The FOS credit hire/repair guidance explains where disputes arise and what “reasonable” looks like.

Staying mobile while you wait (courtesy cars, hire and work realities)

Courtesy car vs credit hire

A policy courtesy car is usually class-limited and depends on availability. Credit hire aims for like-for-like but involves contractual risk if liability or costs are later disputed. Read the FOS credit hire guidance before you sign anything.

Taxi/PHV, van and bike readers

If your vehicle is your income, document urgency and suitability (e.g., PCO-compliant automatic, delivery-ready van, commuter bike with top-box). When you ask for authorisation or mobility support, keep everything proportionate and reasonable—that word matters in every decision.

A natural helper, not a hard sell

If you’re non-fault and off-road in England, Accident Assist Network can coordinate recovery, reputable repairs and like-for-like replacement vehicles (including taxi-plated cars and motorbikes) with explanations in five languages. This is practical facilitation, not financial advice. Learn more on the Accident Assist Network website.

Service note & Mandatory Disclaimer

Accident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. If the at-fault insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Please read every document thoroughly and, if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.”

Need practical help in England?

Call 020 4577 1120 · WhatsApp 07585 300 600 (English · Română · اردو · தமிழ் · हिंदी)

FAQS

Yes. You can usually do so after a non-fault accident if your choice is reasonable on cost/method and you co-operate with authorisation. Insurers must act promptly and fairly: see FCA ICOBS 8.1.

It depends on policy wording and availability. Networks often make cars easier, but if insurer-side delays create loss of use, ask for help and keep a clean log. See the FOS repairs guidance.

No. Credit hire is a separate contract that may be recovered from the at-fault insurer and sometimes gets disputed. Read the FOS credit hire guidance before agreeing.

That’s third-party assistance. It can be convenient but you’re not obliged to accept. Learn how it works in the ABI TPA guide.

You can ask. Approval depends on policy terms, safety and cost reasonableness. Provide a method reference where possible and be open to OE-equivalent parts where appropriate. See the FOS repairs page.