Car Insurance Excess: How to Avoid Paying After a Non-Fault Accident

You didn't cause the crash. You weren't speeding, texting, or running a red light. Someone else hit your car — and now your insurer wants you to hand over £500 before they'll lift a finger.

It feels wrong because it is unfair. In 2025, UK motor insurers paid out a record £11.9 billion across 2.5 million claims, with vehicle damage alone accounting for nearly £7.5 billion (Source: Association of British Insurers (ABI), February 2026). Behind every one of those claims is a real person — maybe a parent juggling school runs, maybe a taxi driver watching £200 a day in earnings disappear — being asked to pay money they shouldn't owe.

Here's what most people don't realise: you may not have to pay your excess at all after a non-fault accident. This guide walks you through exactly what car insurance excess is, why insurers charge it even when you're not at fault, and five proven routes to keep your money where it belongs — in your pocket.

Stressed after an accident? Call 020 4577 1120 for 24/7 help. WhatsApp easier? Text 07585 300 600. We speak English, Romanian, Urdu, Tamil, and Hindi.

Quick Answer: Do You Have to Pay Car Insurance Excess After a Non-Fault Accident?

If you claim through your own insurer after a non-fault accident, yes — you will usually pay your excess upfront and recover it later once the at-fault driver's insurer accepts liability. However, if you use an independent accident coordination route, you may bypass your own insurer entirely and pay no excess at all. Your options depend on evidence strength, liability clarity, and which route you choose. Below, we explain five specific ways to avoid paying excess out of pocket.

Table of Contents

What Is Car Insurance Excess and How Does It Work in 2026?

Car insurance excess is the amount you agree to pay towards any claim before your insurer covers the rest. Every UK motor policy includes it, and it applies to most claim types — whether you caused the accident or not. Understanding how your excess works is the first step to protecting your cash flow.

Compulsory vs Voluntary Excess — What Is the Difference?

Your total excess is made up of two parts. Compulsory excess is set by your insurer based on your age, vehicle, location, and claims history — you cannot change it. Voluntary excess is the additional amount you choose to pay on top, usually to reduce your annual premium.

Compulsory excess typically ranges from £200 to £300 for most drivers, though it can reach £500 to £1,000 or more for younger or higher-risk drivers (Source: money.co.uk). Voluntary excess usually ranges from £100 to £500, though some policies allow higher amounts (Source: Howden Insurance).

Both are added together. If your compulsory excess is £250 and your voluntary excess is £300, your total excess is £550 per claim.

Why Is Your Total Excess the Number That Really Matters?

A growing number of drivers are choosing higher voluntary excess to bring down their premiums. According to a 2023 market study cited by The Independent and GoCompare, 23% of UK drivers now select a £500 voluntary excess — up from 20% in 2022 (Source: Zego / The Independent). That means their total excess can easily reach £600 to £800 or more.

For taxi and private hire drivers, the picture is sharper. Taxi insurance excesses commonly range from £500 to £2,000 (Source: TotalLossGap). Combined with daily income loss of £200 to £220 for London cabbies (Source: LTDA Taxi Earnings Report, via Accident Assist Network), the financial hit is substantial.

Why Do You Still Pay Excess When the Accident Was Not Your Fault?

This is the question that frustrates drivers most — and rightly so. The answer is contractual: your excess is part of your agreement with your insurer, not with the other driver. When you claim on your own policy, your insurer pays out minus your excess regardless of fault. They then pursue the at-fault driver's insurer to recover costs — a process called subrogation (where your insurer recovers money from the party responsible).

If subrogation succeeds, you get your excess back. But this can take weeks, months, or sometimes longer — leaving you out of pocket in the meantime.

What Car Insurance Excess Really Costs a Working Driver

Fictional scenario — for illustration only.

Imagine a London Uber driver — let's call him Tariq. He's rear-ended at a busy rank near Heathrow. His PHV (Private Hire Vehicle, licensed by TfL — Transport for London) is undriveable. His taxi insurer wants £750 excess upfront before they'll arrange anything.

While Tariq waits, he's losing £200 or more every day he's off the road. By day three, the total damage to his pocket is already £1,350 — the £750 excess plus three days of lost income. His insurer has offered a basic courtesy car that isn't TfL-plated, so he can't work with it anyway.

Now picture a parent — let's call her Priya — whose family car is written off at a roundabout. Her insurer deducts £400 excess from the settlement payout. She's now down a car and £400 she hadn't budgeted for, with school runs starting Monday.

Both Tariq and Priya were entirely not at fault. Both are paying for someone else's mistake.

Have you been in a situation like Tariq or Priya? What would you do first — call your insurer, or explore other options?

People Also Ask

Because Asking is the First Step

Do I have to pay my car insurance excess if the accident was not my fault?

If you claim through your own insurer, you’ll usually pay your excess upfront and recover it later through subrogation. You may avoid paying excess entirely by using an independent non-fault route: https://accidentassistnetwork.co.uk/accident-claim-uk-english/

5 Ways to Avoid Paying Car Insurance Excess After a Non-Fault Accident

You have more options than your insurer might tell you. Here are five proven routes — each with clear steps, benefits, and honest limitations.

Ready to get your life back on track? Call 020 4577 1120 now for immediate recovery and replacement hire coordination. Or WhatsApp 07585 300 600 if that's easier. £0 upfront cost.

Route 1 — Claim Directly Against the At-Fault Driver's Insurer

Instead of claiming on your own policy, you can claim directly against the other driver's insurer. This is called a third-party claim, and it means you never trigger your own excess.

You contact the at-fault driver's insurer with your evidence (photos, dashcam, police reference, witness details) and request they cover your repairs and a hire vehicle directly. If they accept liability, they pay — and your own policy remains untouched.

- Benefits: No excess to pay. No impact on your No Claims Bonus.

- Limitations: The at-fault insurer may dispute liability or delay. You'll need strong evidence. You're managing the process yourself.

Route 2 — Use Independent Accident Coordination

Citizens Advice confirms that if the accident wasn't your fault, you can use a credit hire company instead of claiming through your own insurer (Source: Citizens Advice). An independent accident coordination service arranges vehicle recovery, a like-for-like replacement vehicle, and repairs — then recovers costs from the at-fault driver's insurer.

- Benefits: No excess to pay. No impact on your No Claims Bonus. Like-for-like replacement vehicle. Professional drivers can keep working.

- Limitations: This route depends on clear third-party liability. If the at-fault insurer disputes liability or payment, you may become liable for costs under your agreement. Always read every document carefully before signing. The Financial Ombudsman Service outlines these risks clearly (Source: Financial Ombudsman Service).

This is the route that Accident Assist Network coordinates for drivers across England — with £0 upfront cost and fees deducted post-settlement. Learn more about our replacement vehicle service or our recovery and storage options.

Route 3 — Use Motor Legal Protection to Recover Uninsured Losses

Many drivers don't realise their policy includes Motor Legal Expenses cover. This add-on covers the cost of recovering losses not covered by your standard claim, including your excess.

Check your policy documents or call your insurer to confirm whether you have this cover. If you do, a solicitor pursues recovery on your behalf.

- Benefits: Professional legal support at no additional cost if already included.

- Limitations: Many drivers don't know they have this cover. Recovery still takes time.

Route 4 — Ask Your Insurer to Waive the Excess Upfront

Some insurers waive the excess for clear-cut non-fault claims where liability is obvious. This isn't standard practice, but it's always worth asking.

When you report the claim, ask directly: "Given this is clearly a non-fault accident, can you waive my excess?" Provide evidence upfront to strengthen the request.

- Benefits: Simple. Costs nothing to ask.

- Limitations: Most insurers will still charge the excess as standard. There's no legal obligation to waive it.

Route 5 — Excess Insurance

If you're a driver with a high excess — particularly taxi and PHV operators facing £500 to £2,000 excesses — excess protection insurance pays your excess if you make a claim. Policies start from around £24 to £60 per year for standard drivers.

- Benefits: Covers both fault and non-fault claims. Low annual cost.

- Limitations: You need to buy it before the accident. Some policies have exclusions.

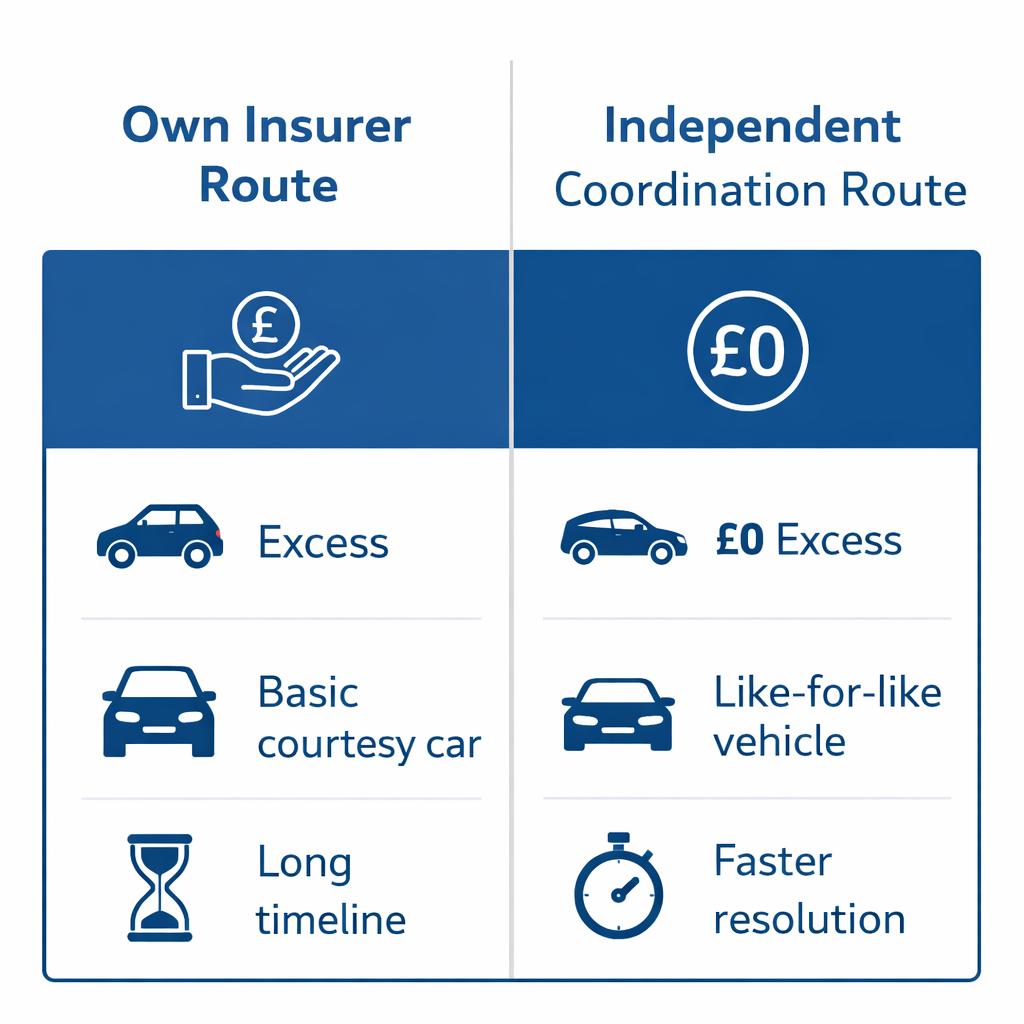

Own Insurer vs Independent Coordination — Side-by-Side

| Factor | Own Insurer Route | Independent Coordination |

|---|---|---|

| Excess payment | Yes — pay upfront, reclaim later | No — £0 upfront in eligible cases |

| Replacement vehicle | Basic courtesy car (if available) | Like-for-like (including taxi-plated) |

| No Claims Bonus | May be frozen until claim settles | Usually unaffected |

| Who manages process | You and your insurer | The coordination service |

| Excess recovery timeline | Weeks to months | No excess charged |

| Professional driver fit | Limited | High |

Important: Both routes have conditions. The independent route depends on clear third-party liability. If the at-fault insurer disputes, costs may fall to you. Always read terms carefully.

People Also Ask

Because Asking is the First Step

How can I avoid paying excess after a non-fault accident?

You can claim directly from the at-fault insurer or use independent accident coordination to avoid triggering your own excess. See like-for-like replacement options here: https://accidentassistnetwork.co.uk/replacement-vehicles/

How Accident Assist Network Can Help After a Non-Fault Accident

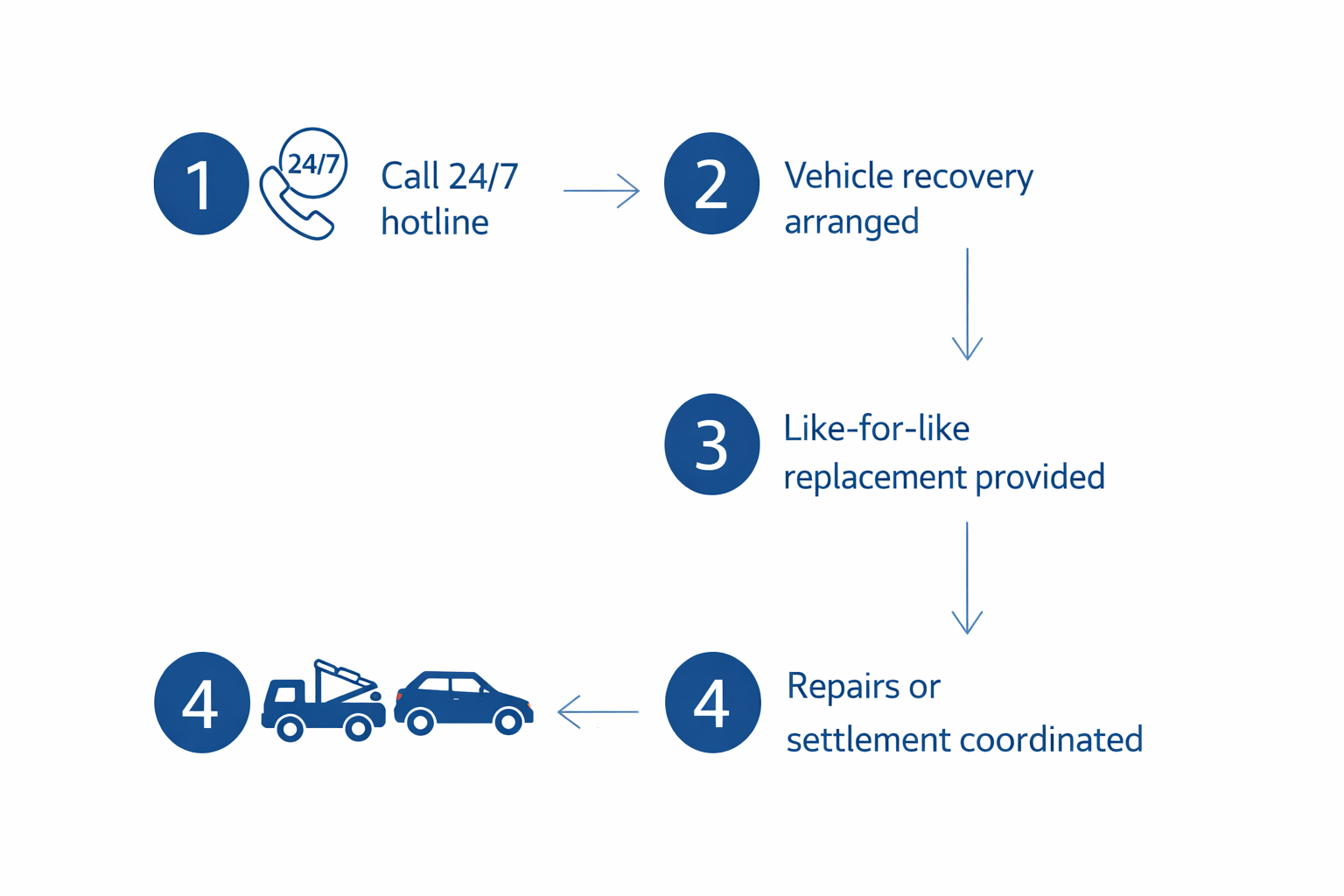

If you've had a non-fault accident and you're worried about paying excess, losing income, or navigating the process alone, Accident Assist Network offers practical, free-assessment coordination across England.

- Free case assessment — Call 020 4577 1120 (24/7) or WhatsApp 07585 300 600. Our team reviews your situation in your preferred language (English, Romanian, Urdu, Tamil, or Hindi).

- Vehicle recovery arranged — We coordinate recovery through our partner network. For London drivers, pickup is typically within 60 to 90 minutes inside the M25. Learn more about our vehicle recovery service.

- Like-for-like replacement vehicle — Where eligible, we aim to provide a comparable replacement within 24 hours — including TfL-plated taxis, courier bikes, and family cars. No excess to pay. Explore replacement vehicle options.

- Repairs or settlement coordinated — An independent engineer assesses your vehicle. You choose between repairs or a cash-in-lieu settlement for total-loss vehicles. Read about repair and settlement options.

Our coordination service operates at £0 upfront cost. A pre-agreed service fee is deducted from the at-fault insurer's settlement.

Important limitation: If the at-fault insurer delays or disputes payment, you may become liable for costs under your agreement with partner companies. We always explain this risk before you sign.

Common Mistakes to Avoid When Dealing With Car Insurance Excess

- Paying excess without questioning it — Always ask your insurer if excess can be waived for clear non-fault claims.

- Not checking for Motor Legal Expenses cover — Review your policy documents.

- Accepting a basic courtesy car when you need a working vehicle — Explore like-for-like options first.

- Delaying evidence collection — Dashcam, photos, witnesses, police references. Collect immediately.

- Signing agreements without reading them — Understand what happens if liability is disputed.

People Also Ask

Because Asking is the First Step

How long does it take to get my excess refunded after a non-fault accident?

Clear cases may refund within weeks, but disputed claims can take months or longer. For immediate recovery and coordination support, visit: https://accidentassistnetwork.co.uk/recovery-storage/

Take Control of Your Car Insurance Excess — Your Next Steps

Nobody should pay hundreds of pounds for an accident they didn't cause. Whether you're a taxi driver watching your earnings disappear, a family driver suddenly without transport, or anyone facing an unexpected excess bill — you have options.

The five routes in this guide give you a clear starting point. Gather your evidence, check your policy, and choose the route that matches your situation.

Call a Trustworthy Friend

We're here 24/7 to walk you through every step.

Visit www.accidentassistnetwork.co.ukAccident Assist Network assists you after a non-fault accident by co-ordinating vehicle recovery, reputable repairs, cash-in-lieu settlements for total-loss vehicles, and like-for-like replacement hire—whether for personal use, licensed taxi work or bike—through our network of independent specialist companies across England. Your one call and we sort it all.

Because our role is one of practical facilitation rather than financial advice, we are not authorised by the Financial Conduct Authority, and our services are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme.

Our partner companies will always endeavour to help you recover costs from the at-fault insurer; however, if that insurer delays or disputes payment you may become liable for credit services or other charges set out in your contract. Each partner company will supply its own terms and conditions in agreements. Please read every document thoroughly and, if anything is unclear, ask us—or an independent adviser—before signing. We are happy to guide you in the language you feel most comfortable with.

Need practical help in England? Call 020 4577 1120 | WhatsApp 07585 300 600

Sources and References

- Association of British Insurers (ABI), "£11.9 billion paid out in 2025 to support motorists across 2.5 million claims," February 2026 — ABI News

- Citizens Advice, "Vehicle insurance if the accident wasn't your fault" — Citizens Advice

- Financial Ombudsman Service, "Credit hire and credit repair services following a no-fault accident" — FOS

- money.co.uk, "How does car insurance excess work?" — money.co.uk

- Zego / The Independent, "Car insurance excess explained (2025)" — Zego Guide

- Howden Insurance, "How much voluntary excess should I pay on car insurance?" — Howden Guide

- TotalLossGap, "Motor Excess Insurance for Taxi & Private Hire Drivers" — TotalLossGap

- LTDA Taxi Earnings Report, via Accident Assist Network — Accident Assist Network

Frequently Asked Questions About Car Insurance Excess

Do I have to pay my car insurance excess if the accident was not my fault?

If you claim through your own insurer, yes — you usually pay your excess upfront. Your insurer then recovers it from the at-fault driver's insurer through subrogation. However, if you use an independent coordination route, you may avoid paying any excess at all. If you're unsure, call 020 4577 1120 for a free assessment.

How do I recover my insurance excess after a non-fault accident in the UK?

You can recover your excess in three main ways: wait for your insurer to complete subrogation and refund it; use Motor Legal Expenses cover if your policy includes it; or claim directly against the at-fault driver's insurer. Check your policy documents first.

What is the difference between compulsory and voluntary car insurance excess?

Compulsory excess is set by your insurer — you cannot change it. It typically ranges from £200 to £300 (Source: money.co.uk). Voluntary excess is the additional amount you choose to pay on top to reduce your premium. Both are added together to form your total excess per claim.

Can I avoid paying excess on a non-fault accident claim altogether?

Yes, in some cases. If you use an independent accident coordination service, costs are pursued directly from the at-fault driver's insurer — so no excess is triggered on your own policy. However, both options depend on strong evidence and clear liability.

How long does it take to get my excess refunded after a non-fault accident?

Timelines vary. Simple cases with clear liability may see excess refunded within a few weeks. Disputed cases can take several months. Online driver forums regularly report waiting six months or longer in complex cases.

Is excess insurance worth it for taxi and private hire drivers?

For professional drivers with high excesses of £500 to £2,000, excess protection insurance can be worthwhile. Policies start from around £24 to £60 per year (Source: TotalLossGap). Given that a single claim could cost you the full excess plus daily income loss, the annual cost is relatively small.

What are uninsured losses and how do I claim them back after an accident?

Uninsured losses are costs not covered by your standard motor claim. These include your policy excess, loss of earnings, travel expenses, and hire car costs. If you have Motor Legal Expenses cover, your legal expenses insurer can pursue these from the at-fault insurer on your behalf. Learn more in our guide on what to do after a non-fault accident.